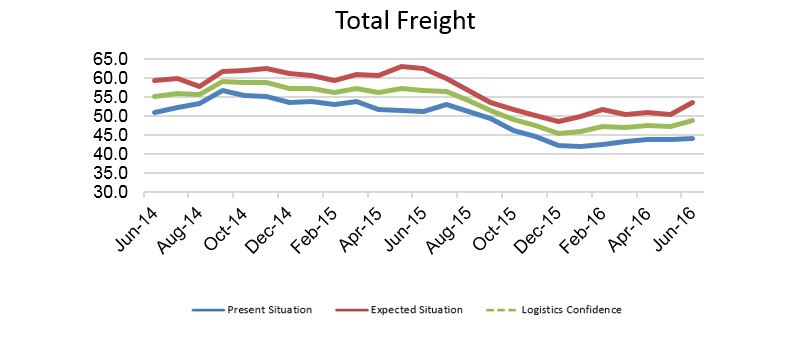

The Stifel Logistics Confidence Index remained negative in June, however, it continued to edge upwards towards the neutral 50 point mark.

Alliances, mergers and acquisitions represent the main points of interest in the global container shipping industry, as consolidation continues. In May, six carriers grouped together to form the ‘THE Alliance’, which includes “K” Line, NKY Line, MOL, Hapag-Lloyd, Hanjin Shipping and Yang Ming Marine Transport.

Moreover, at the start of June, shareholders of United Arab Shipping Company showed support for the company’s likely merger with one of the aforementioned lines; Hapag-Lloyd. The deal will place the resulting entity as the fifth-largest container line in the world, measured by capacity. Meanwhile, third-placed CMA-CGM is expected to consolidate its position with the impending takeover of NOL this month.

Nonetheless, as a result of the current environment of fierce competition amongst carriers, freight rates continue to decline. As stated by Philip Damas, head of the logistics practice of Drewry “this is, for now, resulting in substantial reductions in contract rates for exporters and importers buying under contract.”

While the container shipping industry continues to struggle, the message from IATA is that, “2016 is likely to be another weak year for air freight.” The overall weakness of demand, coupled with continued capacity growth, is likely to continue throughout the year, though the organisation noted that air freight volumes data between March and April showed improvements in all regions bar Latin America.

Whilst aircraft manufacturers are hitting record production rates in response to high demand from airlines, it was interesting to hear the outgoing director of the organisation note that passenger traffic “may be shifting down a gear”. Though passenger traffic growth rates are still likely to remain higher than those in air freight, this is something to observe closely.

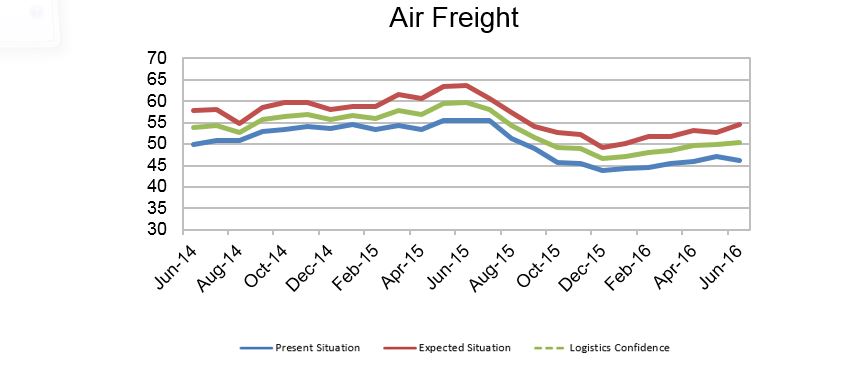

Air Freight

The air freight logistics confidence Index once more gained 0.4 points, totalling 50.4 for June 2016. This is 9.2 points lower than in June 2015, and 3.4 points beneath June 2014.

The present situation results fell by 1.0 points to 46.2. This was principally the result of a 6.0 point fall in the Europe to US lane, which at 48.5, fell below the 50 point mark for the first time since November 2014. Meanwhile, the US to Europe lane declined by 1.8 points to 46.6, and the Europe to Asia lane also contracted slightly, with a 0.3 point fall to 41.8. The only lane to buck the trend was Asia to Europe, which rose by 4.0 points to 48.4.

In a marked contrast, the air freight logistics expectations Index rose by 1.8 points to 54.5, with a 2.8 decline on the US to Europe lane the only contraction recorded. The US to Europe lane improved by 2.2 points to 56.4, whilst the Europe to Asia lane increased 2.8 points to 53.1. The greatest improvement was in the Asia to Europe lane, which rose by 4.7 points to 56.0 for the month.

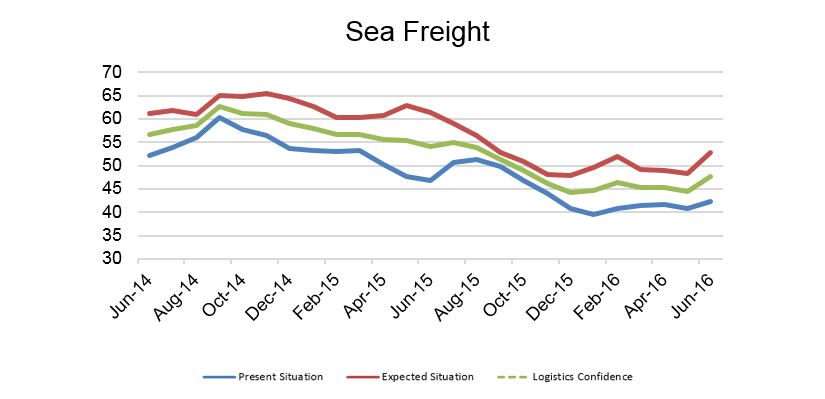

Sea Freight

Sea Freight

For June, the sea freight logistics confidence index improved by 3.1 points to 47.6. This rise was precipitated by an improvement of 1.5 in the present situation index, and growth of 4.6 points in the expected situation index.

Standing at 42.2, the present sea freight index was still negative, as were all four individual lanes surveyed. The Europe to US lane fell by 3.4 points to 48.1, and the US to Europe lane declined by 1.2 points to 40.0. In contrast, the Europe to Asia lane improved by 1.8 points to 34.6. Most significant of all though, and driving through the monthly improvement in the index, was a 7.6 point increase in the Asia to Europe lane, which totalled 46.3 for the month.

Growth in the sea freight expectations index was more pronounced, with gains across the board. This was led by a 6.6 point improvement to 57.3 on the Asia to Europe lane, followed by a 5.9 point gain to 52.3 for the US to Europe lane, and a 4.9 point increase to 48.6 on the Europe to Asia lane. The most minimal increase was registered on the Europe to US lane, which improved by 0.9 points, to 53.2.

One-Off Question

One-Off Question

The June one-off question cited the declining profitability of capacity buying and consolidation, to ask respondents if they believed the provision of value added services to be the next phase of development for the freight forwarding market.

Whilst 23% of survey respondents agreed with the notion that value added services represent the next area of development for the market, almost half (47%) stated that value added services merely represented one of several ways in which forwarders can improve their profitability. Of the remaining participants, 24% believe that there are other priority areas, such as technology, that forwarders can focus on first in their efforts to increase profitability. Only 6% of respondents stated that they did not see the market turning to forwarders for value added services.

Source: Transport Intelligence, July 04, 2016

For more information about the performance of sea and air freight on different trade lanes