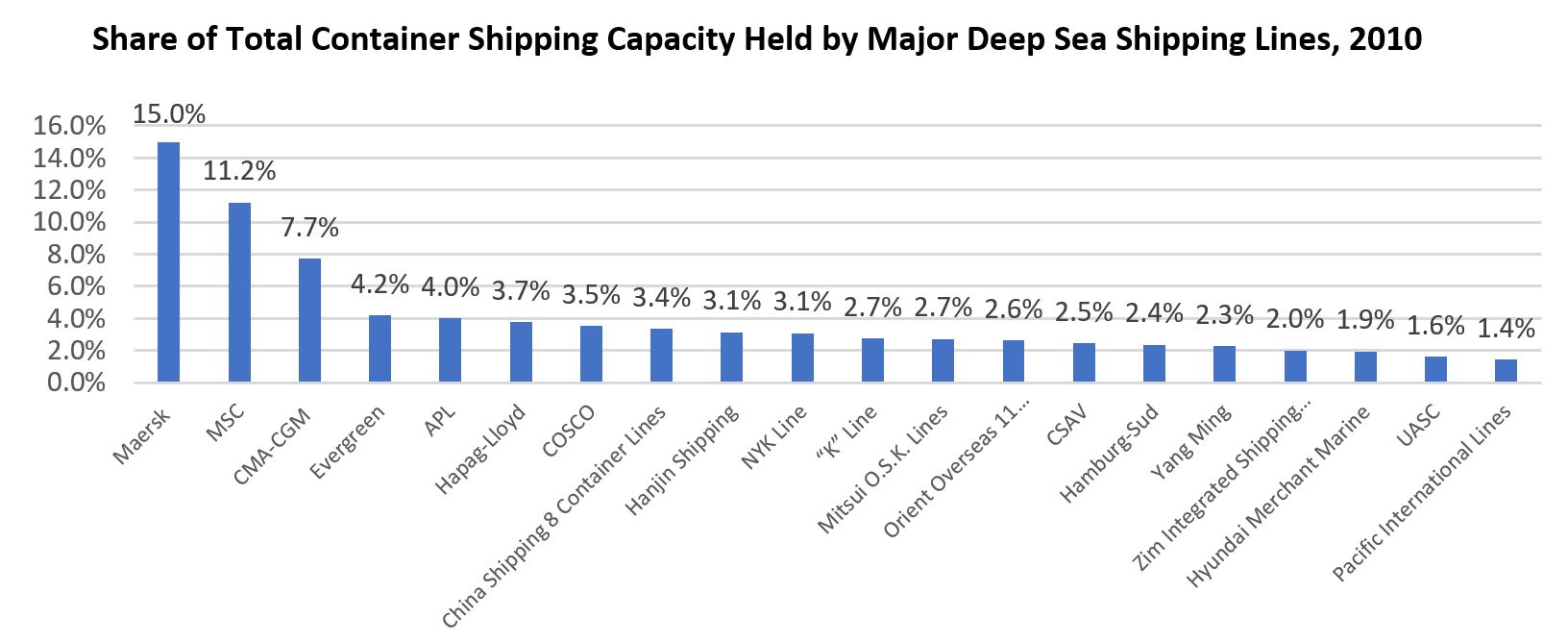

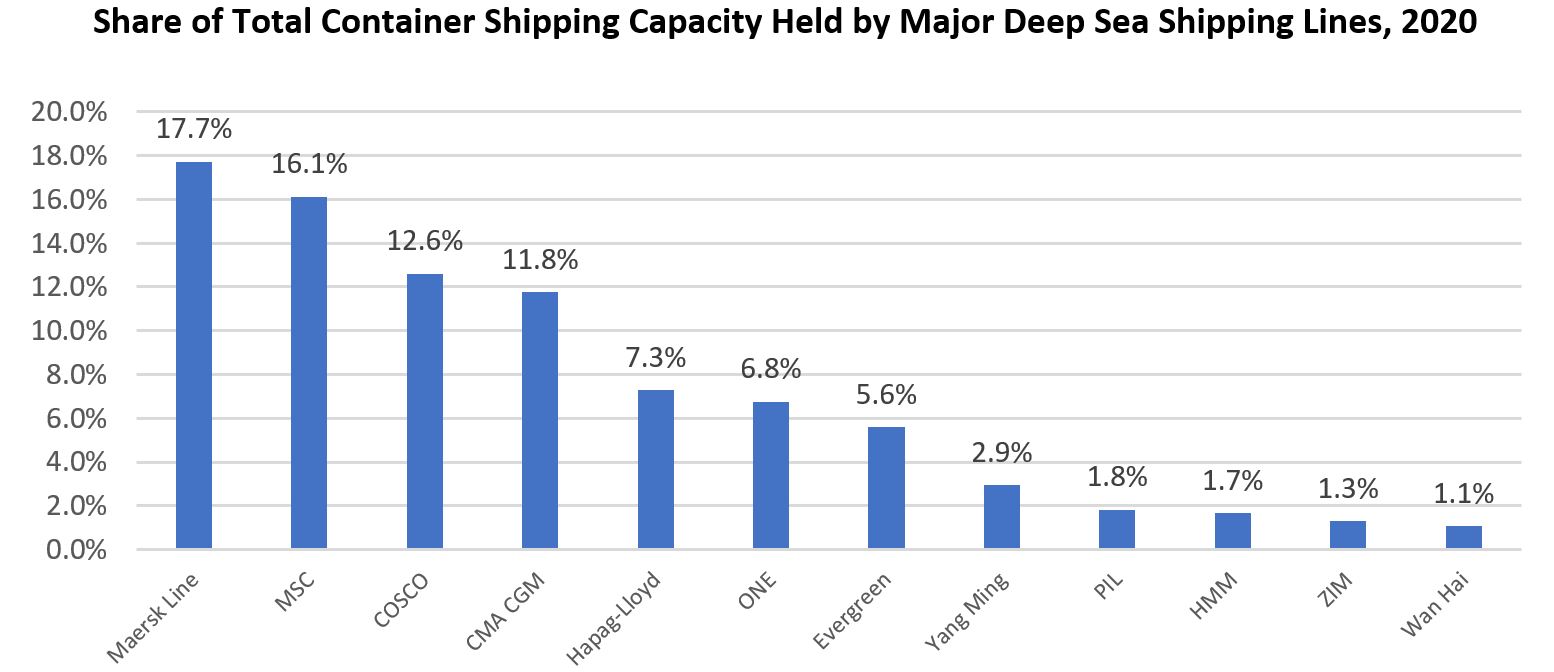

One of the key trends over the past ten years in the container shipping market is the consolidation of the supply-side. As can be seen below, a long ‘tail’ of smaller shipping lines have been acquired by leading companies. This has resulted in a very different marketplace.

Source: NYK

Previous to these consolidations, market equilibrium almost always favoured the customer. Although the leading shipping lines had large fleets, the medium-sized players were always looking to gain market share. In the market for ships, this was easily achieved, with additional capacity financed by chartering vessels from ship-owning companies. Consequently, the option to increase market share by buying ships and offering lower freight rates was usually attractive. Of course, the problem with this approach was that margins and long-term return on capital fell. Indeed, the latter fell to such levels that many of the smaller shipping companies in deep-sea container trades became non-viable. This made consolidation easier.

It is noticeable that rather than the market leaders, Maersk, MSC or even CMA-CGM’s increasing market share, it was middle-market lines that have been successful in the approach of growing by acquisition. For example, Hapag-Lloyd transformed itself from a mid-market player through the acquisition of UASC and CSAV into a more comprehensive and coherent company.

The emergence of ‘networks’ became characteristic of a supply-side that took a different operational method to exploit its assets. This has been seen particularly strongly with Maersk, where the aggressive use of new information architecture seems to have facilitated higher utilisation rates. However, there is some evidence to suggest that the other larger shipping lines have done something similar; evidence such as higher utilisation.

The result is that smaller shipping lines with smaller fleets will be at a disadvantage in the marketplace. They cannot offer the service/pricing ratio that the larger carriers can and their return-on-assets will be lower.

Although ‘shipping conferences’ are meant to deliver some of the capabilities of such a networked approach, they are not as powerful. They retain the infrastructure of the various participants but cannot integrate operations to the degree a single company networked fleet can.

The result of this consolidation has been a change in the structure of competition between shipping lines which in turn is leading to a change in the balance of power between customers and suppliers.

This has not necessarily been expressed directly through the dynamics of negotiations. Indeed, the contrast between the stability of contracts and the volatility of the spot market has been heightened. Rather new market characteristics have been expressed through the ability of shipping lines to reduce the capacity available on the market. ‘Blanking sailings’ was a dangerous tactic formerly, now, however, shipping lines are able to sustain it. This enables them to optimise capacity and indirectly, but powerfully, create a shortage of container slots on the market. The result is that customers begin to chase the container line, enabling the container line to set the price, especially if the service is outside a contract.

This trend is not uniform. Some shipping lines are more aggressive in their blanking of services than others; Maersk for example has been more aggressive than CMA-CGM. This reflects the relative financial stability of the two, however, CMA-CGM is much more stable in 2021 than it was going into 2020, so it will be interesting to observe its behaviour in the short-term.

Lines are buying new ships although these will take time to be introduced. However, if the new market structures are to be effective, the shipping lines will only increase their capacity when the market and their profit margins will be sustained.

Source: Transport Intelligence, March 11, 2021

Author: Transport Intelligence

This brief has been taken from a larger paper, ‘Volatility and Rates in Container Shipping’ by Ti’s senior analyst, Thomas Cullen. The paper is available exclusively to GSCi subscribers. Each week, Ti’s team of senior analysts and industry experts deliver analysis covering the latest logistics and supply chain trends exclusively to users of GSCi.