Global air and sea freight rate dynamics have long been a topic of interest for those involved in international supply chain management. It is well known that since the recession, much of the media coverage around rates has been of the ‘doom and gloom’ variety. This is because rates have plummeted overall thanks to two main factors: the collapse in the oil price and overcapacity in the air and sea freight sectors. But with freight rate dynamics so volatile in the short run and stories coming thick and fast, it is difficult to take stock of the journey the industry has been on over the longer term.

Global air and sea freight rate dynamics have long been a topic of interest for those involved in international supply chain management. It is well known that since the recession, much of the media coverage around rates has been of the ‘doom and gloom’ variety. This is because rates have plummeted overall thanks to two main factors: the collapse in the oil price and overcapacity in the air and sea freight sectors. But with freight rate dynamics so volatile in the short run and stories coming thick and fast, it is difficult to take stock of the journey the industry has been on over the longer term.

Why is it worth taking a look back over the last decade or so? First, we get a clear understanding of how bad things are today compared to before the recession. And second, data reporting has improved over the last 10 years or so such that is now possible to assess how forwarders’ profitability tends to be affected by rate movements.

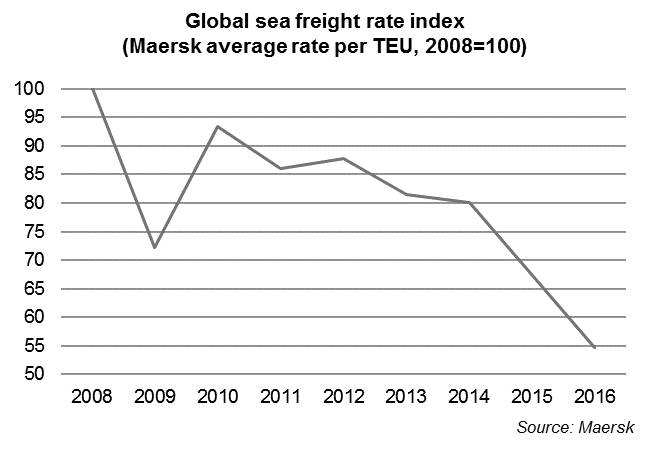

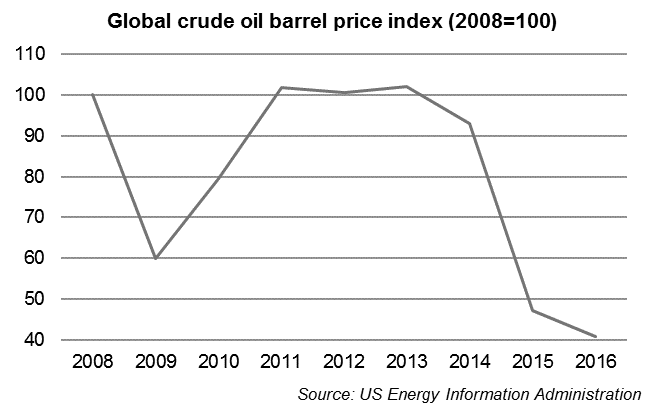

Taking rate dynamics first, the three charts below tell the story. Using Maersk and IATA global freight rate data as proxies for global sea and air freight rates (both measured in dollar terms), both fell drastically in 2009, but then recovered much of their lost ground in 2010. Since then, they have trended down, with the sharpest declines coming in 2015 and 2016. At the end of 2016 average global sea and air freight rates were 45% and 37% lower than in 2008, respectively. Comparing these with the third graph below, it is clear that oil price dynamics (also measured in dollar terms) in 2009 and 2010 heavily influenced air and sea rates, as was the case in 2015 and 2016. However, from 2011 to 2014, rates trended down, as the oil price was generally flat. Over this period, excess supply of carrier space was the primary driver of falling rates.

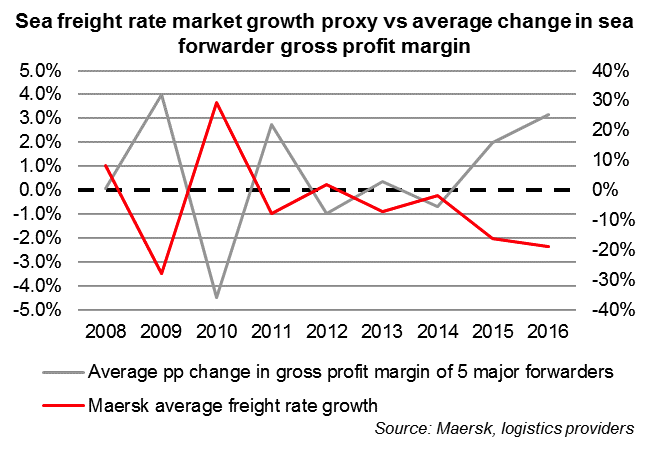

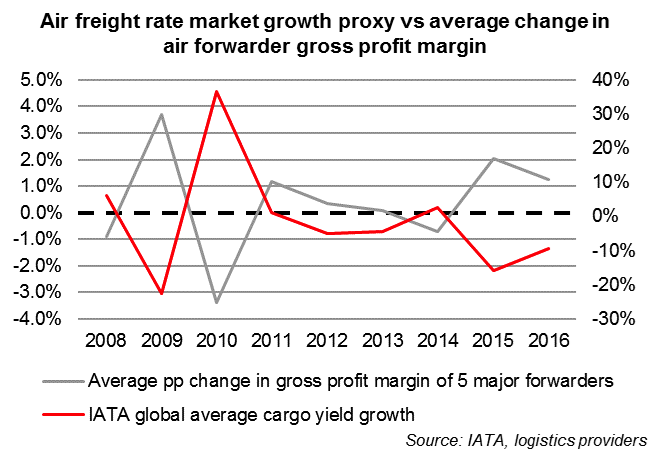

How have forwarders been impacted by this collapse in rates? The two graphs below show that there is a clear negative relationship between carrier rate growth and changes in forwarders’ gross profit margins that has held for about the last decade or so (read change in gross profit margin off the left axis and freight rate growth off the right). As rates fall, forwarders’ gross profit margins tend to increase, and vice versa. This applies for both air and sea freight. Every one percentage point gain in sea freight forwarder gross profit margin is, on average, associated with a six percent decline in rate growth. For air, the corresponding figure is five percent. Gross profit margin here is the difference between forwarding revenues from customers and the cost paid to carriers divided by revenue from customers. The average change in gross profit margin is calculated as per the financial results of five major forwarders which offer the figures: Expeditors, DSV, DHL Global Forwarding, Panalpina and Kuehne + Nagel. While every forwarder’s set of figures is slightly different (as presented in Global Freight Forwarding 2017), the underlying negative relationship for each provider is actually strikingly similar across the board.

How do such dynamics arise? When carrier rates fall, forwarders’ buy rates from carriers decline in line rapidly. However, forwarders’ sell rates to their customers do not fall as quickly. This is, among other reasons, due to contract structures.

For example, Deutsche Post DHL’s first quarter 2017 report, stated: “Due to our contract structures the air freight price increases compared with last year can only be passed on to customers with a delay.”

In Expeditors’ 2016 annual report, they warn that: “Volatile market conditions can create situations where rate increases charged by carriers and other service providers are implemented with little or no advance notice. We often times cannot pass these rate increases on to our customers in the same time frame, if at all.”

With sell rates not falling as quickly as buy rates, this drives up gross profit margins. So are falling rates good for forwarders and higher rates bad? Not really. Gross profit margins increase in times of falling rates because forwarders do not pass on the lower rates to their customers immediately. If you imagine a situation where rates subsequently stayed constant for the next year or so, then those lower rates would largely be passed on to customers and gross profit margins would fall. Any gain would therefore be largely transitory and illusory.

In any case, a comparison of gross profit margin levels of the five aforementioned forwarders over the last decade reveals relatively small differences. The difference between buy and sell rates is not where the game is won. Where differences can really be found is in seeing how good forwarders are at turning their initial gross profit into underlying operating profit (see Global Freight Forwarding 2017).

The key operational performance metric for forwarders is therefore the conversion ratio (EBIT divided by gross profit). What really drives differences in this is variation in staff and management quality, overheads, technology, innovation, strategy and value-added services etc. Just last year, two of the five aforementioned forwarders had conversion ratios for their whole forwarding operation of around 10%, while two others had figures of over 30%. Evidently, this is where we see who is leading the pack, and who is trailing behind.

Source: Transport Intelligence, July 4, 2017

Author: David Buckby

To find out more about Global Freight Forwarding 2017, or Ti’s expertise in the freight forwarding market, including analysis of its market size and forecasts broken down by regions and countries, strategies of the major 3PLs, analysis of technologies in the industry and more, click link below or contact Ti’s Business Development Manager, Michael Clover.

Logistics briefing is a FREE service providing: