Bath, UK, 3rd of November 2022 – Diesel prices, driver shortages and drought in Europe have all played a significant role to push average European road freight rates up again in Q3 despite lower consumer spending. However, data from the end of the quarter shows prices softening towards the end of Q3.

The European Road Freight Rates Benchmark Report, produced by Transport Intelligence, Upply and IRU, takes an in depth look at road freight rates across Europe on a quarterly basis. It explores the indicators and trends driving change – from fuel increases to global events – and provides an outlook for the road freight market to support the decisions of shippers, transport providers and hauliers.

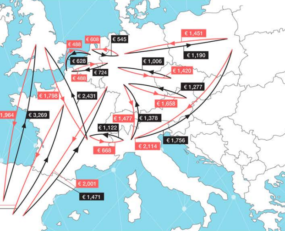

Report highlights:

Thomas Larrieu, Chief Executive Officer at Upply, comments: “In a context of global inflation, the European climate is marked by weakening demand and consumption. This is slowing down the increase in road freight rates, but it is not reversing the trend. Indeed, road carriers are facing workforce shortages that are affecting the amount of capacity available, as well as an increase in their overall costs. The Upply data show a growing gap between spot and contract prices. More than ever, shippers have an interest in favouring long-term contracts in order to secure their capacity and obtain competitive rates from carriers.”

IRU Senior Director of Strategy and Development Vincent Erard adds: “Drivers are a critical factor in keeping essential supply chains moving, something we saw clearly during the pandemic. Now, logistics operators and freight rates in many countries are threatened by another looming crisis: the growing shortage of this invaluable human resource. People are at the heart of this challenge. We must continue pushing efforts and investments boost the attractiveness of the driver profession, especially to young people, and make it easier for people to qualify and join the driver pool.”

Ti’s Head of Commercial Development, Michael Clover, says: “International European Road Freights rose to a new peak in Q3 but, as we look ahead at what will be a difficult winter right across Europe, we can see freight rates begin to soften through September and October as volumes begin to drop. Looking forward, we expect this softening in rates to continue over the next couple of quarters.”

About the European Road Freight Rate Benchmark

The European Road Freight Rate Benchmark report is designed to provide greater visibility of freight rate development across Europe. It will be available to download from Wednesday 3rd August.

Click here to download a copy of the full benchmark report

If you have any questions about the report please contact Michael Clover, Ti’s Head of Commercial Development: [email protected]

About Transport Intelligence (Ti):

Ti is the world’s leading source of market intelligence for the logistics and road freight industry, providing data and analysis through its European Road Freight Transport report series, Global Supply Chain intelligence (GSCi) database and expert consultancy services. www.ti-insight.com

Media contact: Michael Clover

Head of Commercial Development

+44 (0)1666 519907

About Upply:

Upply is a technology platform that provides benchmarking tools for road, sea and air freight rates (including past data and forecasts). Upply collects several million invoices every week from the world’s leading shippers, forwarders and carriers. This data is aggregated, anonymised and made available to our users to assist them in their decision making. Launched in 2018, the company is based in Paris and currently has over 50 employees.

www.upply.com

Media contact: Gwendydd Beaumont

Communication Manager

[email protected]

+33 (0)6 10 72 98 57

About IRU:

IRU is the world road transport organisation, promoting economic growth, prosperity and safety through the sustainable mobility of people and goods. As the voice of more than 3.5 million companies operating mobility and logistics services in all global regions, IRU leads solutions to help the world move better.

www.iru.org

Media contact: John Kidd

Senior Adviser, Public Affairs

+41 79 386 9544

[email protected]