The market for air and sea freight has been characterised by significant disruption and dysfunction since the onset of the global Covid-19 pandemic in 2020. Entering 2022, the picture remained one of high demand and even higher rates in both ocean and sea freight.

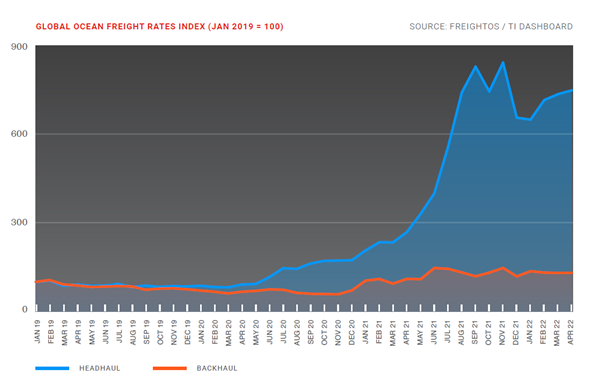

There has been an expectation for the sky-high ocean head haul freight rates to return to a pre-pandemic normal, and with a significant dip in rates leading into 2022, there was promise that rates could continue downwards throughout the year. As shown in Ti’s Ocean Freight Rate Tracker: Q2 2022, the first quarter of the year has at least delayed these hopes for now. Rates have risen from the dip in Q4-21 and continue to rise into the opening month of Q2-22. Backhaul rates also continue to remain somewhat elevated from their pre-pandemic levels.

Volume, despite already being at high levels, has generally continued to rise in Q1-22, especially on the west coast. Oakland saw volumes grow 13.2% compared to the previous quarter, and Los Angeles and Long Beach volumes grew 7.3% and 7.5% respectively. This continues to lead to port congestion, a major contributing factor in the stubbornness of high rates in Q1-22. Data from Statista shows that on average 11.1% of global shipping capacity was lost to congestion in 2021, up from 2.3% in 2019. This is still rising in Q1-22, with congestion causing 12.7% of global capacity to be lost on average in January.

Rising bunker fuel prices have also driven up costs for carriers, which can exceed half of the running costs for larger vessels. Global average prices for bunker fuel are up 38.0% in April from the start of the year, adding upwards pressure on rates.

There are hints that the conditions for rates to finally begin their descent are being set. While Covid lockdowns in China may cause disruptions on their own, this may begin to provide some limited yet much-needed relief from the congested ports on the west coast and also the now increasingly congested east coast as well. The extent of this relief however may not be enough to change the direction of rates. High inflation has also been damaging consumer confidence, with April 2022 reporting inflation in the Euro area at 7.5%. This alongside the war in Ukraine has caused The OECD’s European Consumer Confidence Index in Q1-22 to end 2.5 points lower than the Q4-21 average. This will likely result in a fall in demand, although the effects of this may take some time to be reflected in sea freight rates.

Those involved in the shipping industry do not think Q2-22 will mark the beginning of the end for high sea freight rates. Ti’s Ocean Freight Confidence Index, which tracks shippers’ and carriers’ expectations on rate developments, was just below the 50-point mark by the end of April, indicating an expectation of moderate increases in rates in the coming months. However, the proportion of respondents that believe rates were going to ‘significantly increase’ fell by a third between January and April, suggesting that many are seeing upward pressures now weakening.

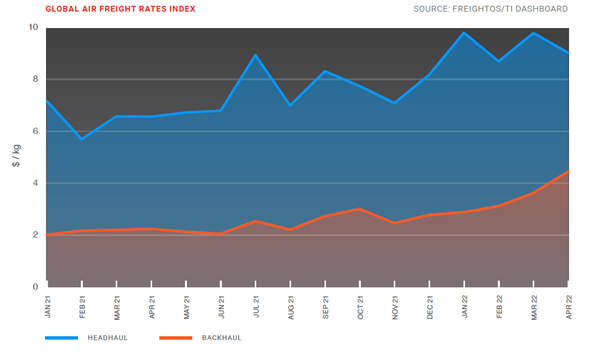

Air freight rates have similarly been elevated throughout the pandemic by supply side issues, with discussion also centred around when the return to pre-pandemic levels will occur, although as described in Ti’s Air Freight Rate Tracker: Q2 2022, this does not appear to be soon. Both head haul and back haul rates have been trending upwards ever since the start of 2021. Head haul rates ended in April 2022 at $9.02/kg, $2.29 higher than in April 2021. Increases on back haul rates have been rising through Q1-22 and into April.

Capacity in air freight has continued to increase after the massive recovery at the start of 2021. The return of capacity has allowed the pent-up demand for air freight over 2020 to begin to release. In this environment of increasing capacity and built-up demand being relieved, it would not be unreasonable to expect a fall in rates. There are several explanations as to why this has not been the case. The war in Ukraine and subsequent sanctions and restrictions has had impacts on capacity on the transatlantic lane and has caused major disruption on the East Asia – Europe lane. Jet fuel spot prices have been increasing since the start of 2022, in part influenced by the conflict. Chinese Covid restrictions have caused further disruptions on the transpacific lane. There has also been a significant sea to air shift in response to disruptions and congestion in sea freight.

While it is true that rates in air freight react quicker to external factors than in sea freight, the issues causing continued upwards pressure in rates are not set to improve in the short term. The war in Ukraine appears to currently have no end in sight, the Chinese government is adamant to adhere to its zero Covid policy, and sea freight disruption continues.

Ti’s Air Freight Confidence Index has dropped by an average of 43 points from March to April. While this still means the consensus is a rise in rates in the coming months, expectation has shifted away from significant increases to moderate increases. This potentially reflects the expected reduction in upwards rate pressure due to the fall in consumer confidence, which should impact demand of air freight services quicker than in sea freight.

It appears to be the case that when considering the mix of factors driving ocean freight, the direction of ocean rates in Q2-22 will see little change from the previous quarter. Although more volatile, a similar picture is presented for air freight rates in Q2. However, the growth prospects for major economies does look increasingly pessimistic, with the possibility of a global recession in the second half of 2022 becoming more likely. If this is the case, the retraction in demand might just provide what is needed to at last set freight rates on course towards pre-pandemic levels.

This Brief provides a snapshot of Ti’s latest coverage of freight rate developments. An extended coverage of the supply chain challenges highlighted above are available in Ti’s Ocean Freight Rate Tracker Q2 2022 and Air Freight Rate Tracker: Q2 2022.

Source: Transport Intelligence, May 19, 2022

Author: Connor Wyse