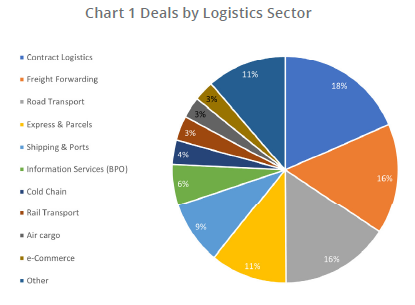

Looking at Ti Insight’s M&A database, it becomes apparent which sectors have seen the most activity over the past 25 years and highlights what role state players have played in consolidation. Accounting for almost two thirds of deal volumes, the four largest industry segments, are Contract Logistics, Freight Forwarding, Road Freight and Express and Parcels. The volume of contract logistics companies acquired shows the appetite for more value-adding and higher margin operations.

Of the fours sectors mentioned, ‘Express and Parcels’ is by far the smallest in terms of market size, and consequently the number of deals is, in relative terms, much greater than that in the other sectors. One of the reasons for this apparent disparity is that all the major express companies as well as many Post Offices have been highly acquisitive. In order to build scale quickly, these companies have bought multiple smaller domestic competitors, which have subsequently been integrated into global or regional networks. The same is true of M&A in the road freight/trucking sector. Both in Europe and in the US, multiple acquisitions have been made to build out groupage/less-than-truckload networks.

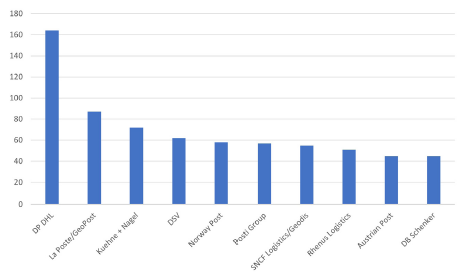

Deal volumes by major logistics player

The Ti database shows how many of the industry’s biggest deal makers themselves became consolidated into even bigger, more aggressive conglomerations. For example, we can see that UK-based but global logistics player Tibbett & Britten was acquired by Exel, which in turn was acquired by Deutsche Post DHL. Between them, these three companies alone comprise 245 separate companies, showing not only the scale of the acquisition effort, but also the challenge of dealing with the integration of these entities into a coherent and focused organisation.

Of course, deal volume is not everything. Many of the companies bought, for example, by the Nordic post offices, have been relatively small express parcels operators. Some companies have preferred to make a small number of very large deals, which allows them to avoid the sometimes painful process of integration. Even this strategy is not fool proof. As was highlighted in the previous paper on M&A, Japan Post’s rush to buy Toll Group made the management blind to the underlying problems within the company.

The role of state players in consolidation

The chart below also shows the extent to which the public sector has been involved in the consolidation of the industry, mainly through either postal or rail organizations. The leading publicly fully, partly or formerly owned market consolidators include, but are not limited to, Deutsche Post (DHL), Deutsche Bahn (DB Schenker), La Poste (GeoPost/DPD), Japan Post, Post Nord, Royal Mail (GLS), Russian Railways (Gefco) and Swiss Post.

By owning some of the world’s largest transport and logistics players, the role of the state has gone way beyond merely providing the structure in which companies can operate (i.e. ‘setting the rules of the game’). As we have seen, many of these state-owned players have not been content just to participate in markets – they have actively transformed them by acquisition programmes either using public money or at the very least leveraging their borrowing power.

In the past, the role of government in the supply chain and logistics industry has waxed and waned along with the prevailing political sentiment of the time and the present situation is no different. On one hand, post-Covid, governments will be desperate for revenues to prop up ailing national accounts and consequently could be minded to sell off their assets. On the other, the control which ownership of very large transport and logistics assets provides could allow politicians to influence corporate strategy where it intersects with public policy. For example, in matters relating to employment, investment or environmental behaviour, the latter being particularly important.

Whilst all sectors of the global logistics industry have undergone radical consolidation in the past 25 years, for the main, the sector remains highly fragmented. With the exception of a few markets, even the largest players command a relatively small market share and this will mean that the pace of transactions is unlikely to slow. Deals will be driven by the quest to, among others, increase economies of scale, enhance buying power (especially in the forwarding industry) and build out global networks. At the same time, new targets will continue to come onto the market due to, e.g. failing management, market pressure, and obsolescent IT. PE companies will continue to play a role in identifying short/medium term opportunities to leverage assets and create scale players whilst moving in and out of the market at regular intervals.

Given the shifting market dynamics influencing the development of the logistics and supply chain sector, it seems inevitable that the companies which make up of the upper echelons of the industry will be very different in ten years’ time from those which dominate today.

Source: Transport Intelligence, March 4, 2021

Author: Transport Intelligence

This brief has been taken from a larger paper, ‘M&A Activity in the Global Logistics Industry – Part 3’ written by Ti’s CEO, Professor John Manners-Bell, and senior analyst, Thomas Cullen. The paper is available exclusively to GSCi subscribers. Each week, Ti’s team of senior analysts and industry experts deliver analysis covering the latest logistics and supply chain trends exclusively to users of GSCi.