With Lloyd’s List recently publishing its annual report on the top 100 global ports by container throughput, it is a good time to take stock of throughput growth in the recent past, present and future. It seems appropriate to characterise 2016 as a pretty poor year, and 2017 as a very good year, whilst 2018 looks to be somewhere in between.

Starting with 2016, using the figures from Lloyd’s List’s One Hundred Ports, throughput growth was about 2% in the year.

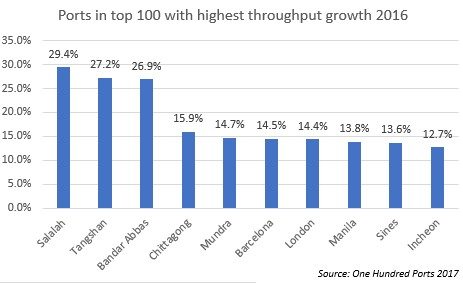

Looking at some of the winners and losers, the highest throughput growth belonged to Salalah in Oman. The transhipment hub reported TEU growth of 29.4% in 2016, though the previous year its volumes contracted by 15.3%. It is in competition with other ports for such volumes and as such it is easy to see why volumes can fluctuate quite wildly year-on-year. In fact, several of the top 10 fastest growing ports primarily have greater transhipment volumes to thank for their high growth performance, including Tangshan, Barcelona and Sines.

As for Bandar Abbas in Iran, throughput growth of almost 27% came on the back of the lifting of sanctions, prompting many container lines to resume services. Currently handling around 3m TEUs per year, it has plans to expand capacity to 9.8m TEUs by 2020.

Elsewhere, Chittagong, which handles about 90% of Bangladesh’s containers (dominated by fashion/textiles), recorded impressive growth of 15.9%.

Meanwhile Manila reported throughput growth of 13.8% in 2016, on the back of economic growth of 6.8%. The Manila International Container Terminal accounted for almost half (2.2m TEUs) of national throughput, and reported growth of 10.8%. Port investment appears to be contributing to the strong numbers. ICTSI, which owns and operates the terminal, introduced an online container booking platform in October 2015. Moreover, the company improved terminal capacity by 18% through completion of a storage yard in November 2015. ICTSI is building a seventh berth and ordering 25 cranes to allow the terminal to handle ships with capacities of over 13,000 TEUs.

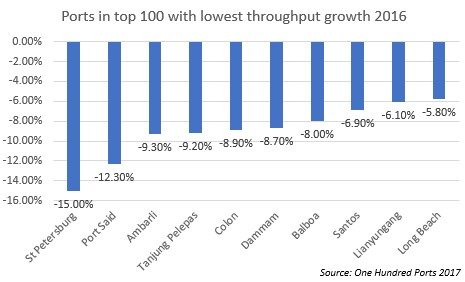

As for those suffering volume declines, St Petersburg’s throughput tumbled by 15% in 2016 to less than 1.5m TEUS, on account of sanctions and a weak Russian economy.

Port Said’s throughput decrease of 12.3% in 2016 is not really telling of the state of the Egyptian economy, but of the loss of Suez Canal related volumes to the Panama Canal.

At first glance, this explanation seems at odds with the two Panama Canal ports of Balboa and Colon also reporting volume contractions, of 8.0% and 8.9% respectively. However, while the expanded Panama Canal has permitted the transit of larger vessels, according to One Hundred Ports, “it has reduced the need for hub and spoke operations in the region”. The slowdown in the growth of global box trade also was partially to blame.

Another emerging market to suffer was Brazil, as South America’s biggest port, Santos, reported a decline in throughput of 6.9%. This came on the back of GDP falling by 3.6%. The fall in value of Brazil’s currency, the real, also appeared to have a net negative effect.

Ti’s forecasts for 2017 volumes on emerging market trade lanes also suggest some big winners and losers. Calculated as part of the upcoming Agility Emerging Markets Logistics Index, they suggest 2017 has been a far better year for emerging markets trade lanes than 2016. Cumulatively, ocean freight export tonnage to the US and EU is forecast to increase by 7.9%, while imports are expected to be flat, though containerised tonnage is doing considerably better.

Looking ahead, the big question is whether 2018 volume growth will be similar to what we’ve seen in 2017 (Alphaliner data suggests global container throughput increased by 6.7% in the first six months of the year).

Linton Nightingale, the editor of One Hundred Ports, suggests not, stating: “Box traffic may have surged in the first half of 2017 – prompting revised forecasts of unprecedented 5% or even 6% full-year volume growth – but that will prove to be an anomaly. Moderate demand growth could return as early as next year.”

Neil Davidson, Drewry senior analyst for ports and terminals, has stated: “The message is not to get too carried away with potential 2017 growth, as in 2018 we will probably be back to our normal 3% or 4% growth level.”

That seems like a reasonable central estimate. The biggest downside risk probably relates to China. If a sudden tightening of global financial conditions exposes financial fragilities, there is a possibility of a sharp slowdown. That really would wreck global port throughput growth.

Source: Transport Intelligence, November 23, 2017

Author: David Buckby