The parcels market in China is unlike anywhere else in the world. Its consumers or netizens (“net citizens”) have taken to e-commerce with great verve, drawn in by successful early starter e-retailers, rapid delivery times and low prices. The scale of the market makes it stand out too. By volume, China’s parcels market is nearly 5 times larger than the United States.

But the development of the market has created intense competition. The market is dominated by the “Tongda” companies – YTO, STO, ZTO, Best and Yunda, in addition to premium operator S.F. Express and China Post. In a bid to gain market share, the operators are locked in a price war which has, according to the China State Post Bureau, seen average parcel prices fall by 57.1% over the past decade.

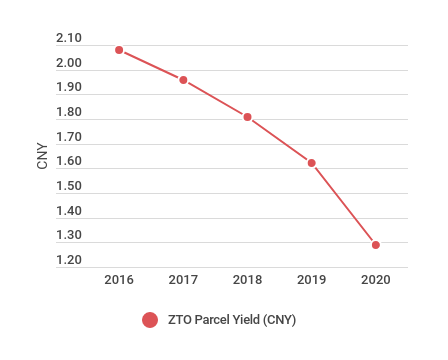

ZTO claims to be the market leader in terms of volumes. Over 90% of its parcels are attributable to e-commerce platforms, with Alibaba a major stakeholder. Since 2016, ZTO has seen parcel yields drop from CNY 2.08 ($0.30) to a staggeringly low CNY 1.29 ($0.19). Note however that ZTO effectively only runs a parcel network, whilst outsourcing collection and delivery to “Network Partners” who charge consumers directly for last mile services. These partners are seeing revenues squeezed too.

Revenue/Piece at ZTO

Source: ZTO/Ti Calculations

Incredibly, on such low revenue/piece, ZTO still returns a gross profit. The company’s unit cost of revenue was CNY 1.06 ($0.15) over 2020, leaving a gross margin on parcels of 17.8%. The company also made $663.1m in net income in the year.

ZTO has managed to find cost savings in recent years through a number of avenues, enabling it to continue producing a profit. In 2017, it began to increase the use of longer 15m-17m trailers used in its line haul fleet. These trucks now account for 81% of their vehicles, up from 39% in 2016. Increasing automated sort capacity also appears to have provided efficiency gains. With just 8 automated sorting lines in 2016, that number increased to 339 in 2020. This appears to have helped with labour costs too. Despite volumes rising at a CAGR of 39.4% over this period, employees in its Sorting division only increased at a CAGR of 5.6%.

As well as business decisions, other entities have shaped the market in China to varying degrees. ZTO has benefitted over the past year from the federal toll fee waiver during the pandemic and lower domestic diesel prices. Both of these costs are influenced at least to some extent by the Communist party, which holds significant influence over the shape of any market in China.

Lower priced parcels also crucially benefit Alibaba, a company that many of the parcel providers rely on heavily for volumes. Significantly, it also has minority stakes in a number of the Tongda providers and has included them into its Cainiao logistics ecosystem. The continued price war benefits Alibaba by making e-commerce products more attractive.

Due to the influence of such significant entities in the market, making predictions around its future is challenging. However, the situation of ever-decreasing parcel prices is unlikely to persist over the medium term. Additional efficiency gains look set to become harder achieve, with margins being squeezed towards breaking point. Diesel prices are under pressure to increase in the short term, whilst labour costs in China are continuing to rise sharply. However, prices have continued to fall in recent quarters and do not look to have bottomed out yet. This will make the situation ever more challenging for China’s parcel companies in its unique market.

Source: Transport Intelligence, July 27, 2021

Author: Andy Ralls