The Coronavirus pandemic continues to ravage the air freight market and uncertainty persists as pricing, capacity and demand experience volatile times. The end is currently not in sight and the potential vaccine is triggering concern as distribution is questioned. Despite this, there are signs of recovery, though only small and slow.

In late September, The International Air Transport Association (IATA) released its Monthly Air Cargo Market Analysis with data from August 2020. The Ti Dashboard has been recording three sets of data from this publication since January 2013; International Air Freight Market CTK Year on Year Growth, International Air Freight Market Available CTK Year on Year Growth and International Cargo Load Factor (CLF) Year on Year Growth.

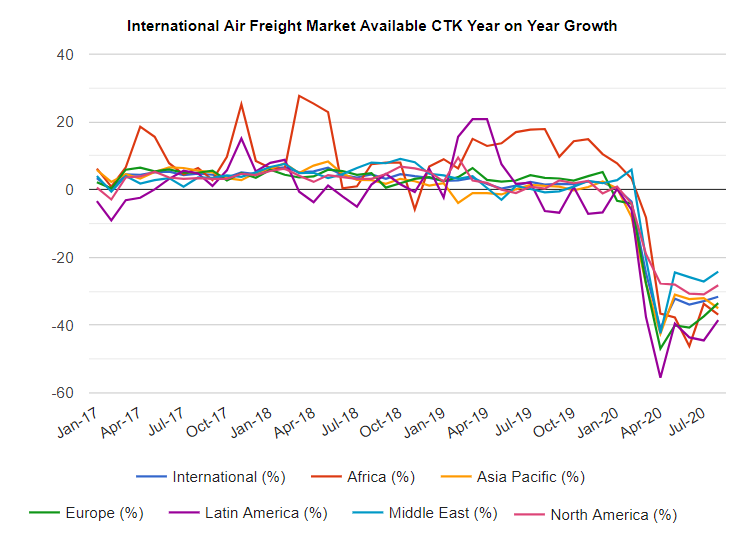

The Ti Dashboard of the month is International Air Freight Market Available CTK Year on Year Growth which has data going back to January 2017. The graph shows how impactful the Coronavirus has been on available cargo tonne-kilometres (ACTKs) across the world.

Source: IATA/Ti Dashboard

From February this year, the shocks linked to the virus can be seen starting across the world, namely in the Asia Pacific region where ACTKs fell by 8.1% year-on-year. However, over the first half of the year, the situation worsened. By April, when much of the world was locked down, International ACTKs were down 40.9% on April 2019, Asia Pacific had fallen further to 42.5% but hardest hit, of the whole year to date, was Latin America with 55.5% fewer ACTKs than the same month in 2019. April was the trough of the year as by May the world began to slowly emerge and whilst ACTKs were still hugely down compared to 2019 they had improved from the month before.

As of August, the most recent data, the association reported figures that showed whilst air cargo traffic is recovering, insufficient capacity is slowing the process. The rebound in cargo volumes has been slower than expected, mostly because air cargo capacity remained limited, with industry-wide available cargo tonne-kilometres (ACTKs) declining by 29.4% in August. International belly capacity was still scarce, and airlines had not been able to raise dedicated freighters capacity as much as is required. Air transport also lost market share of global trade due to competition from cheaper ocean transport, a typical pattern during downturns but not what is usually experienced at the start of an economic upturn.

Looking ahead, while seasonality has been muted so far since the start of the crisis, the standard peak season for air cargo is due to begin in the coming weeks and as ocean rates increase and delays follow this might provide some support to volumes. The launching of delayed products such as the iPhone 5G and the PlayStation 5 or even a potential vaccine may contribute to a stronger end to the year but the constrained capacity due to reduced passenger flights mean prices are expected to rise.

Source: Transport Intelligence, October 6, 2020

Author: Holly Stewart

The Ti Dashboard is a collection of global and regional transportation, trade and economic data, which includes key metrics regarding the air freight and forwarding markets. The Ti Dashboard provides the facts you need in one easy to use source, saving you time, with insight and analysis from industry experts that enable you to make informed decisions. For more information, click here.