The e-commerce market is seemingly facing ever more stringent demands from consumers as the years go by. They want online orders delivered faster, through a multitude of delivery channels and returns are increasingly common. On this basis, it is tempting to think that the logistics cost burden for online retailers should be on an upward trend.

Yet this is not necessarily the case. First of all, some terminology. Logistics cost burden here means ‘logistics costs as a proportion of online sales’, not just logistics costs. Of course, as an online retailer expands, its logistics costs are bound to increase over time as it processes higher volumes which obviously incurs greater costs. But will these costs grow faster than sales? If so, then logistics costs as a proportion of online sales will increase. If costs grow by less than sales, then the proportion will go down.

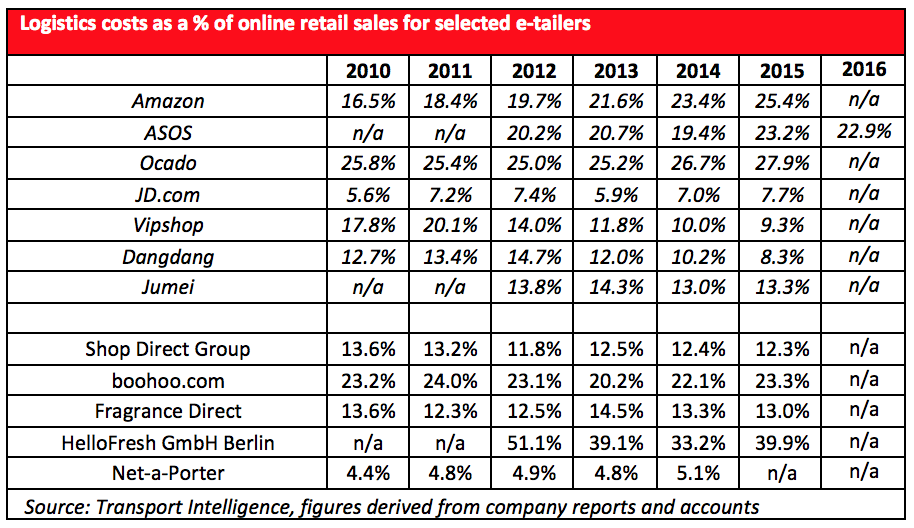

The table below displays the trends in logistics cost burden for various online retailers. It is worth noting that logistics cost burden is not the same to all people, at least not in the way that it is reported. Most e-tailers seem to include both fulfilment costs (primarily costs incurred in operating and staffing warehouses) and outbound shipping costs in their definition, although some appear to only measure outbound shipping costs. Inbound shipping costs are rarely included.

Note: Data in italic in the table is for companies whose logistics costs encompass both fulfilment costs and outbound shipping costs. Meaningful comparisons can be made across companies. Data not in italic is for companies which provide data for their ‘distribution costs’. It is not clear whether this just covers outbound shipping costs or includes other costs too.

Regardless of the definitions used, what is interesting is that the logistics burden for an array of companies is not definitively rising over time. In fact, among the companies listed here, only Amazon’s logistics burden is clearly increasing since 2010. Of the years when their logistics burden has fallen, Chinese players such as JD, Vipshop, Dangdang and Jumei have cited economies of scale and switching towards regional or local couriers as reasons driving down their cost burden. Also of note is that the logistics burden is typically much lower for Chinese players compared to e-tailers operating in developed economies – thanks largely to relatively lower labour costs both in terms of staffing warehouses and effecting deliveries. This gap in costs could well narrow however. JD warned in both its 2014 and 2015 annual filings that it anticipates its logistics burden will increase, thanks to rising Chinese labour costs.

Outside China, the comments made by some retailers are particularly interesting. In its 2016 annual report, ASOS asserted that its distribution costs as a proportion of sales increased by 30 basis points to 14.9% thanks to its operation becoming more global overall, with EU free returns and US standard delivery days adding to costs. However warehousing costs fell by 60 basis points to 7.9% of revenue thanks to the full year effect of new automation technology leading to better efficiency at is main UK warehouse. Elsewhere, Ocado’s logistics burden benefitted from better operational efficiency at several of its sites and improved delivery drop density, though its logistics burden still increased overall. Clearly, there are many factors at work.

So what conclusions can be derived? Firstly, it is very difficult to tell for any particular e-commerce logistics market – be it China, the UK or the US – whether the logistics burden is on the rise or not. Secondly, once a company has an established operation, its logistics burden tends not to fluctuate too much year-on-year.

It is these notions that have driven the forecasting approach in Ti’s report, Global e-commerce Logistics 2016. For any country, three scenarios are presented for its e-commerce logistics market – one where the logistics burden is constant over the course of the forecast, another where it has increased, and another where it has decreased. Given the uncertainty regarding the direction of travel of the logistics burden, such an approach seems the most sensible to take.

If this brief has been of interest you might also like to download Ti’s Global e-commerce 2016 report. The report contains Ti’s bespoke market size and forecasting data, as well as overviews of some of the world’s leading e-commerce businesses. In addition, the report includes company profiles of both post offices, LSPs and dedicated e-commerce solution providers to showcase the different strategies shaping the market we know today. Ti will be publishing it’s 2017 version of the report early next year, for more information, contact Michael Clover, [email protected]

Source: Transport Intelligence, December 7th, 2016

Author: David Buckby