Even though some of the regulations have now been adopted, controversy and opposition remain around the Mobility Package. Issues surrounding insufficient infrastructure to enable the successful implementation of the regulations and environmental concerns, among others, continue to linger.

The European Commission commissioned two studies to assess the expected impacts of two specific aspects of Mobility Package I, the return obligation and cabotage quotas. A scenario approach was developed to represent the potential market responses to the return obligation and derive the impacts on transport activity, the environment and congestion.

Overall, the results from the studies suggest that the return obligation for lorries and the quotas imposed on combined transport operations are likely to have negative effects on transport activity and the environment.

Impact on CO2 emissions

Critics of the Mobility Package have also been pointing out a possible clash between the new regulation and the EU’s ambitious Green New Deal plan, since the requirement for trucks to return to their home base on a regular basis is likely to result in increased CO2 output and endangers environmental goals of member states’ agendas.

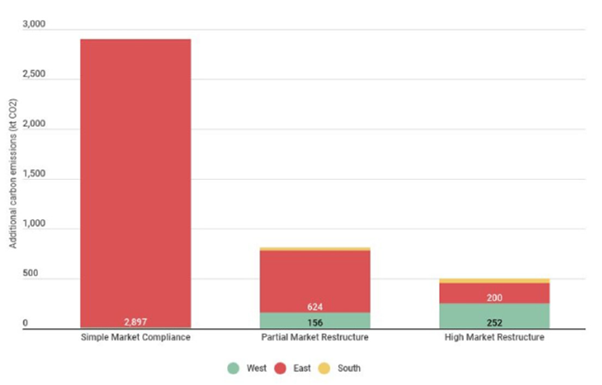

The analysis of the return obligation for vehicles shows that in the simple market scenario, the rule is likely to create additional journeys, potentially resulting in up to 2.9m tonnes of additional CO2 emissions in 2023 (a 4.6% increase in international road freight emissions). Across the three scenarios that were studied, the increase in CO2 emissions ranges from 0.8% to 4.6%.

In addition, costs of air pollution due to negative health effects and other damages were estimated at €25.9m associated to an increase in NOx and PM2.5 emissions in 2023 under the simple market compliance scenario. For the restructuring scenarios, these costs are expected to range between €4.5 and €7.2m.

Additional carbon emissions per scenario for each MS cluster group, 2023

Source: Ricardo

The study focusing on the cabotage quotas for international combined transport operations estimates that a widespread use by Member States of the option to introduce them could lead to an additional 397,000 tonnes of CO2 emissions and to potential negative long-term effects on rail and intermodal freight.

Considering the results of both studies, the two provisions could therefore result in up to 3.3m additional tonnes of CO2 emissions annually, which is comparable to a year’s worth of total transport emissions in Estonia. They could also generate up to 704 tonnes of nitrogen oxides (NOx) and 251 tonnes of particulate matter (PM2.5).

The Commission’s intention is to open a discussion with Member States, the European Parliament and all concerned parties on the possible ways forward, based on the data and findings of the two studies.

The Commission aims to have an open dialogue to assess potential next steps in the light of the need to pursue the Green Deal objectives.

Source: Transport Intelligence, September 2, 2021

Author: Transport Intelligence

This brief has been taken from a larger paper, ‘The Impact of Mobility Package on European road freight operations’ by Ti Insight. This paper is available exclusively to GSCi subscribers. Each week, Ti’s team of senior analysts and industry experts deliver analysis covering the latest logistics and supply chain trends exclusively to users of GSCi.