The express and parcels market has witnessed explosive growth in shipments over the past decade. This has been caused by the shift in shopping preferences towards e-commerce and away from physical stores. Whilst this has been a positive for the global market, the increasing mix of B2C parcels has brought about its own challenges, and in some markets, growth in parcel yields (revenue/shipment) has been stagnant.

United States

Pioneers UPS and FedEx are considered to be some of the most successful shipping companies anywhere in the world. They have dominated the US parcels landscape for decades, with only the Postal Service rivalling their networks. Achieving such network scale is vital to a successful national parcel operation and creating a viable model is no small feat. DHL notably tried unsuccessfully to penetrate the US market, but effectively ended domestic operations in 2009. A number of regional players also exist, but none have expanded to match the service offerings available from UPS, FedEx and to an extent the USPS. However, Amazon’s growing logistics network is challenging the incumbents. Whilst it remains a key customer for UPS and the USPS, it effectively operates its own in-house parcels network, whilst increasingly making use of its Delivery Service Partners and (to a lesser extent) Flex schemes to provide last mile services.

With only four major providers in the market, the incumbents have been able to justify price rises over the past decade. The data below is taken from a US Postal Regulatory Commission report. It indicates that the major players in the market have been able to increase prices substantially in recent years.

Source: US Postal Regulatory Commission

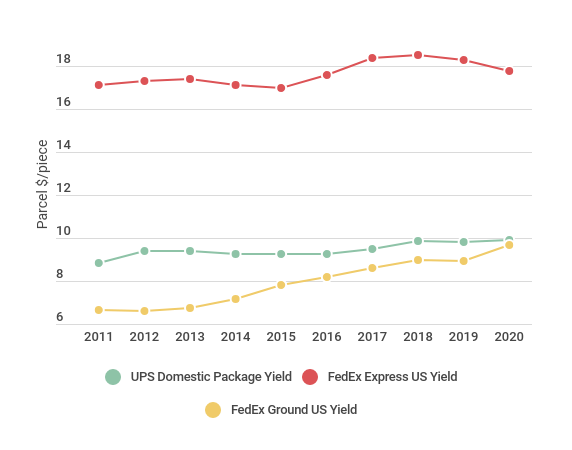

However, that has not always translated into higher average revenue/shipment across the companies. The graph below shows how yields have changed over time at UPS and FedEx. These changes do not always match the price hikes as outlined above. UPS yields have increased at a CAGR of 1.3% per year over the last decade, whilst FedEx Express yields increased 0.4% a year and its Ground yields increased 4.3% per year. The past decade has also seen rapid growth in the number of B2C e-commerce parcel shipments. At UPS, B2C accounted for 64% of volumes in 2020, whilst at FedEx, the figure was 67% for fiscal 2020. It appears that a shift in the mix towards lower yielding volumes has effected average revenue per piece.

Source: Company Annual Reports and Ti Calculations

Germany

Competition in Germany is much more fierce than in the United States. Although national hero DHL dominates in terms of market share (>40% by its own estimates), a number of other players are present in the field. For UPS, Germany provides the next largest revenue source outside of its home market. The same can be said for the UK’s Royal Mail subsidiary, GLS. Hermes, part of e-commerce behemoth Otto Group, is also a significant player and claims to deliver around one third of B2C parcel deliveries in the country. DPD claims to be the second largest provider in the German parcels market. FedEx, in part through its TNT acquisition, has a significant presence in the country, whilst Amazon is growing its last mile network. Its recent moves saw DHL close a parcel centre in anticipation of a newly opened Amazon sorting centre, only to backtrack later. The company operates its Delivery Service Partners scheme in Germany, but has recently begun recruiting drivers directly for last mile deliveries in some cities.

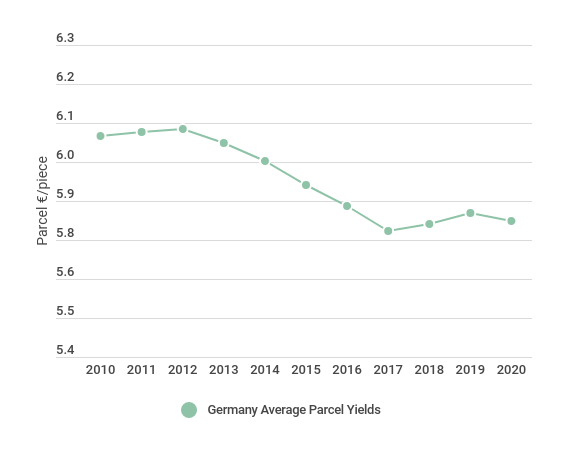

As a result of this intense competition and due to the increase in B2C volumes over time, yield performance in Germany has been weak. According to data from express and logistics association BIEK, the average parcel in Germany was worth 4.1% less in 2020 than in 2010.

Source: BIEK

However, like in the US, it is important to note how B2C volumes are a key cause of weakening revenue/piece. B2B volumes can yield approximately 90% more revenue than B2C shipments in Germany. Despite B2C volumes being associated with higher failure rates, which increase costs, they are generally much lighter (typically under 2kg) which allows for better capacity utilisation. Further, B2B volumes can have less stringent delivery expectations than B2B and businesses are more likely to pay a higher price for time-definite delivery than consumers. Therefore, the increasing share of B2C within the overall parcels mix is likely to lead to weaker yields.

Lessons for other markets

On the surface, it appears parcel providers operate in an increasingly more challenging environment, where efforts to expand networks and increase service offerings do not lead to higher yields. This is not necessarily detrimental to providers within the market, since B2C volumes can lead to greater network utilisation and shipments are typically lighter, which lowers the cost base.

Nevertheless, in markets where competition is more intense, achieving yield gains is challenging for existing operators. Moves by Amazon to penetrate more of the parcels market will only intensify this competition further.

Source: Transport Intelligence, August 26, 2021

Author: Andy Ralls