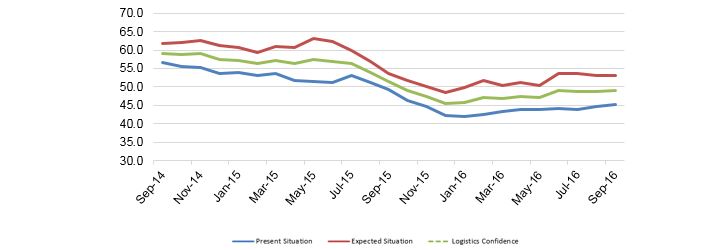

A weak trend of improvement in the Stifel Logistics Confidence Index is evident, though the Index is still short of the neutral 50 point mark.

With a fourth consecutive month on month increase registered in September, the Index for sea freight has shown that confidence appears to be creeping back into the industry, despite the well-cited capacity crisis. Unfortunately for Hanjin Shipping, this has not translated into enough container volumes for the carrier to survive; it filed for bankruptcy on August 31st.

Ironically, time may prove this event to be the turning point for the container shipping business. With a round of M&A activity initiated by several major carriers late last year, competition in this commoditized market has increasingly descended into a scrap over who can best sustain losses.

Should the South Korean Government elect not to intervene on behalf of Hanjin Shipping, the company’s death may well serve as a stay of execution for other carriers under financial pressure. According to the Journal of Commerce, Hanjin Shipping accounted for 7.85% of trans-Pacific containers inbound to the US during the first half of 2015. Moreover, the shipping line accounted for around 9% of Asia-Mediterranean trade during the same period. Accordingly, the Shanghai Shipping Exchange measured a 51% increase in the spot rate for shipping a 40-foot container from Asia to the US West Coast last week, to $1,746 per FEU.

It is logical to assume that this price rise, along with the general disruption to shippers, could incentivise many customers to switching their products to air freight transportation, as with the West Coast labour dispute of 2014. The CEO of Atlas Air did note that “It [the bankruptcy] could mean opportunities for air freight.” Nonetheless, he also suggested that the situation could change dramatically with the prospect of Government intervention.

Total Freight

Air Freight

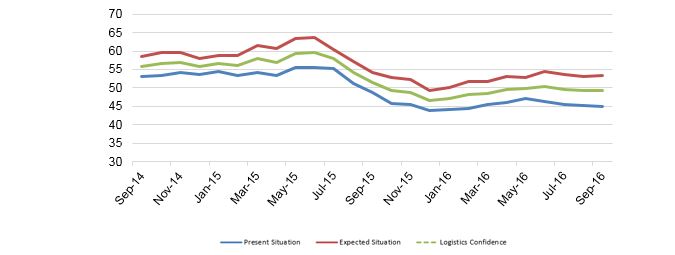

The overall Air Index recorded a 0.1 point rise, taking it to 49.3 for September. The current Index was down by 0.1 points to 45.1, whilst the expected Index rose 0.3 points to 53.5. The marginal overall gain was driven by a slight improvement in the expected situation.

For the current air freight situation, lanes between Europe and Asia recorded poor performance, whilst those between Europe and the US achieved gains. Europe to Asia was down slightly, by 0.1 points to 42.8, with a more significant fall of 1.5 points to 45.0 on the Asia to Europe lane. By contrast, the Europe to US lane improved by 0.1 points to 46.7, with the US to Europe lane rising 1.0 points to 46.1.

For the expected situation, all but one of the lanes surveyed noted month on month improvements. The exception was Europe to Asia, which fell by 3.2 points to 46.4. Meanwhile, Asia to Europe increased 0.8 points to 56.5, and US to Europe improved by 0.9 points to 55.2. The most significant gain was recorded on the Europe to US lane, which rose by 3.3 points to 56.2.

Air Freight

Sea Freight

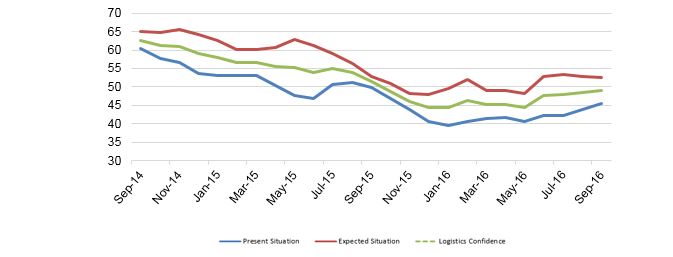

The Logistics Index for sea freight noted a minor increase of 0.6 points to 49.0. The expected Index fell by 0.2 points to 52.6, though this was offset by the 1.4 point increase in the present Index, which rose to 45.4.

The increase depicted in the present Index for sea freight was the result of gains across three of the four lanes. The outlier amongst the surveyed lanes was Europe to US, which declined by 0.6 points to 45.6. Meanwhile, Europe to Asia and Asia to Europe both recorded gains of 1.6 points, producing totals of 40.3 and 50.1, respectively. The most marked gain came on the US to Europe lane, which increased by 3.3 points to 45.3.

The minor decline displayed within the expected Sea Freight Index was due to a mixed set of results amongst the lanes. Falling by 1.3 points to 54.8, the performance of the Europe to US lane drove the result, whilst the Asia to Europe lane also fell, by 0.7 points to 54.0. Somewhat offsetting the downward trend, Europe to Asia gained 1.1 points to total 49.8, though this was not enough to arrest the overall decline, as the US to Europe lane remained unchanged at 51.8.

Sea Freight

One-Off Question

The September one-off question, asked, given the industry’s capacity crisis, whether or not we have seen the last orders for Ultra Large Container Vessels (18,000+ TEU).

A majority of respondents (57.1%) stated that orders of ULCVs are likely to halt in the short-term, until volumes begin to increase once more.

Moreover, a significant proportion of the respondents (28.6%) asserted that there is no reason to think that ULCV orders will stop. Only 9.2% of the survey participants argued that ULCVs have had their day. The remaining 5.1% of respondents provided a range of perspectives, including the contention that the price of oil is a key determinant.

Source: Transport Intelligence, September 22, 2016