The Logistics Confidence Index has rebounded from the slight dip experienced in March, with Present Index scores demonstrating a continuation of volume growth.

This appears to tally with the recent results from leading players involved in global freight movements. In recent filings, UPS, C.H. Robinson and Kuehne + Nagel all reported volume increases in their freight forwarding businesses for the first quarter of the year. The latter recorded a striking set of results, with Air Freight volumes up by 16%, and Sea Freight up by 9%.

Take part in next months survey

Meanwhile, the latest IATA monthly results (for February) recorded an 12% year-on-year increase in Freight Ton Kilometers. Following on from an increase of 8.4% in January, IATA’s Director General Alexandre de Juniac has stated that this warrants “cautious optimism”, with yields rising. Nonetheless, he has cited “the current protectionist rhetoric” of leaders in several countries as a very real ongoing concern.

Within the sea freight industry, another carrier appears to be foundering. On April 20, Yang Ming, the world’s ninth largest container shipping line, suspended trading on the Taiwanese stock exchange until 4 May. The carrier has been the subject of intense scrutiny for a while due to its financial position; the company is loss-making, with a debt to equity ratio of 482%.

A crucial difference between Yang Ming and the collapsed Hanjin Shipping is that the Taiwanese Government has offered financial support to keep the company afloat. Yang Ming has reiterated this to investors and media, but shippers are nonetheless starting to avoid the carrier over fears that the events of last year will repeat themselves. Yang Ming’s losses were reduced in the fourth quarter of 2016, but the company’s problems illustrate that whilst the sector as a whole is beginning to tackle its capacity issues, we are not out of the woods yet.

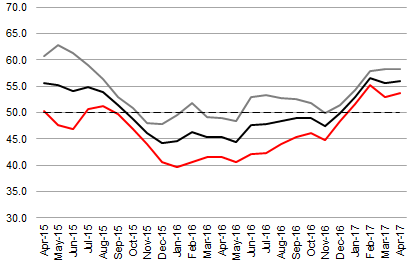

Logistics Confidence Index: Air and Sea Freight

Air Freight

The Air Freight Index registered a month-on-month rise of 0.6 points to 53.0 for April 2017. Whilst this score reflected a year-on-year improvement of 3.4 points, it stood 4.0 points below the April 2015 total.

The Air Freight Logistics Situation Index noted a month-on-month improvement of 1.5 points to 53.0. Month-on-month changes were driven by a strong performance on the Europe to Asia lane, which saw a 4.4 point improvement to 57.8. Nonetheless, two other lanes also recorded gains over the same timeframe; Asia to Europe, which noted a 0.9 point gain to total 57.4, and US to Europe, which improved by 0.5 points, though at 46.6, still remained in negative territory. Europe to US was the only lane to record a decline, falling by 0.6 points to 48.3.

The performance of the Air Freight Logistics Expectations Index was decidedly more mixed, with two lanes displaying gains, and two recording losses. Europe to US was the most significant mover month-on-month, with a 6.2 point decline to total 46.2. A more moderate decline was seen on the US to Europe lane, which fell by 3.1 points to 46.8. In contrast to these results, expectations were strong for Asia to Europe, which was up by 4.8 points to 63.5, and also for Europe to Asia, which scored 53.6 following a 2.2 point improvement.

Logistics Confidence Index: Air Freight

Sea Freight

The Sea Freight Logistics Confidence Index recorded an overall score of 56.0, having increased by 0.4 points against the previous month’s score. The result was 10.7 points greater than the score registered in April 2016, and 0.4 points below that recorded in April 2015.

Standing at 53.7, the Sea Freight Logistics Situation Index improved by 0.8 points against the previous month. This result was driven by a significant monthly improvement in one lane, Europe to Asia, which improved by 6.4 points. This was the only lane to note an improvement, with declines registered on the Asia to Europe (down 2.5 points to 60.4) and US to Europe (down 1.8 points to 44.2) lanes. The Europe to US Lane was unchanged, with a score of 50.7.

The Sea Freight Logistics Expectations Index was unchanged from March, totaling 58.2. This outcome was derived from a mixed performance amongst the lanes surveyed. Whilst Europe to Asia saw a points increase of 1.7 to 57.7, Asia to Europe declined by 2.0 points to 65.5. Similarly, the US to Europe lane improved by 4.2 points to 55.1, whilst the reverse lane, Europe to US, declined by 1.8 points to 53.1.

Logistics Confidence Index: Sea Freight

One-Off Question

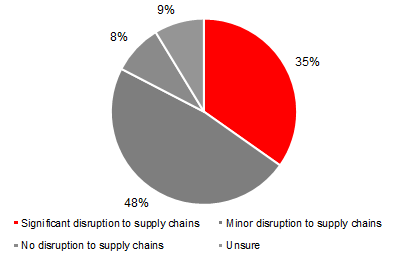

For this month’s one-off question, respondents were asked the following: “What level of disruptive impact will the launch of the new shipping alliances on April 1 have upon supply chains?”

Unsurprisingly, the vast majority of respondents predicted supply chain disruption of some kind. The largest response group, containing 48% of participants, anticipated minor disruption; the second-largest group, comprising 35% of responses, predicted significant disruption. The remaining respondents were split almost evenly between those who foresaw no supply chain disruption (9%), and those who were unsure of what to expect (9%).

What level of disruptive impact will the launch of the new shipping alliances on April 1 have upon supply chains?

You are invited to take part in this monthly survey, all participants are sent the results of the index when published as well as the chance to win $100 Amazon vouchers if you take part in 3 months consecutively.