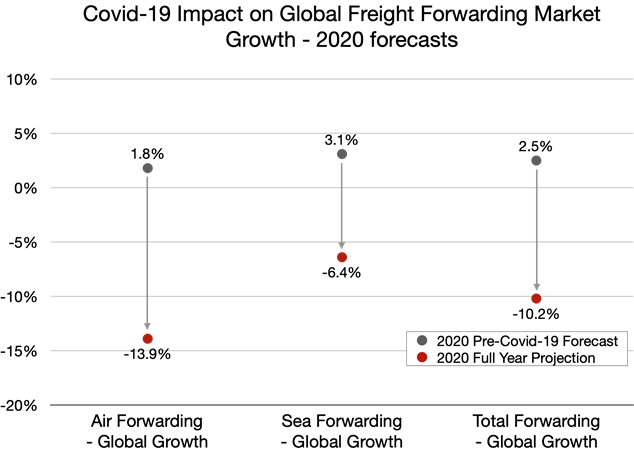

Ti’s latest market projections for 2020 show that the market will contract by 10.2% year-on-year, the worst fall since the financial crisis. Over the first half of 2020 the global freight forwarding market contracted by 11.6% year-over-year in real terms. A more positive second half of the year is expected as the global economy reopens following the easing of lockdown restrictions, but the picture remains bleak across air and sea forwarding.

Over the course of 2020, the fall in the global air freight market is expected to be -13.9%. This is the largest annual contraction since the global financial crisis in 2008-2009. It is also the second consecutive year of global air forwarding contraction – 2019 saw the market shrink 4.1% in real terms as the US-China trade war and a slowdown in global automotive sales began to bite. Over the first half of 2020, the global air forwarding market shrank 15.3%. Although the pace of contraction looks set to slow in the second 6-months of 2020, there are no guarantees, particularly as a second-wave of Covid-19 infections looks perilously close in Europe and North America.

The story is similar but less extreme in the global sea forwarding market. Ti’s market sizing data shows a 7.6% contraction in H1 2020, with the full year projection again lessening the fall to 6.4%. Sea forwarding has seen stable and steady growth over the last decade with expansion rates in around the mid-single digits. Growth was also positive in 2019, despite headwinds from a growing wave of protectionist policies on key east-west trade lanes.

It will come as no surprise that the global forwarding market will take a considerable real terms hit in 2020. Both volumes and capacity have both been severely impacted by the Covid-19 crisis. As the virus circulated in China initially, its manufacturing output dropped substantially. This weakened intra-regional trade volumes and exports to major consumer markets (notably the US and Europe) fell considerably. As the virus spread further, these major import markets saw their own industries shutdown, along with vast swathes of retail, at a time where China was recovering. The subsequent loss in trade output in the first half of the year was stark.

Andy Ralls, a Quantitative Analyst at Ti said: “It has been a challenging, but not disastrous period for both air and sea freight forwarders. Volumes have plummeted, but finding capacity, particular on airlines, has been extremely challenging. This tightness has given forwarders the chance to pass on high rates to shippers, leading to strong revenue growth. The next few months will be difficult with the shape of the global economic recovery still highly uncertain. In all likelihood, the pattern of recovery across different geographies will vary, meaning forwarders will need to be flexible to deal with shippers’ needs.”

Ti’s new market projections break down growth in the freight forwarding market by mode, region and country with growth rates provided for H1 and the full year 2020. CLICK HERE to download the whitepaper.

If you would like to access Ti’s full dataset on the freight forwarding market then you can take a look at Ti’s Global Supply Chain intelligence (GSCi): https://www.ti-insight.com/product/gsci/

Source: Transport Intelligence, October 1, 2020

Author: Transport Intelligence

_________________________________________________________________________________________________________________________________