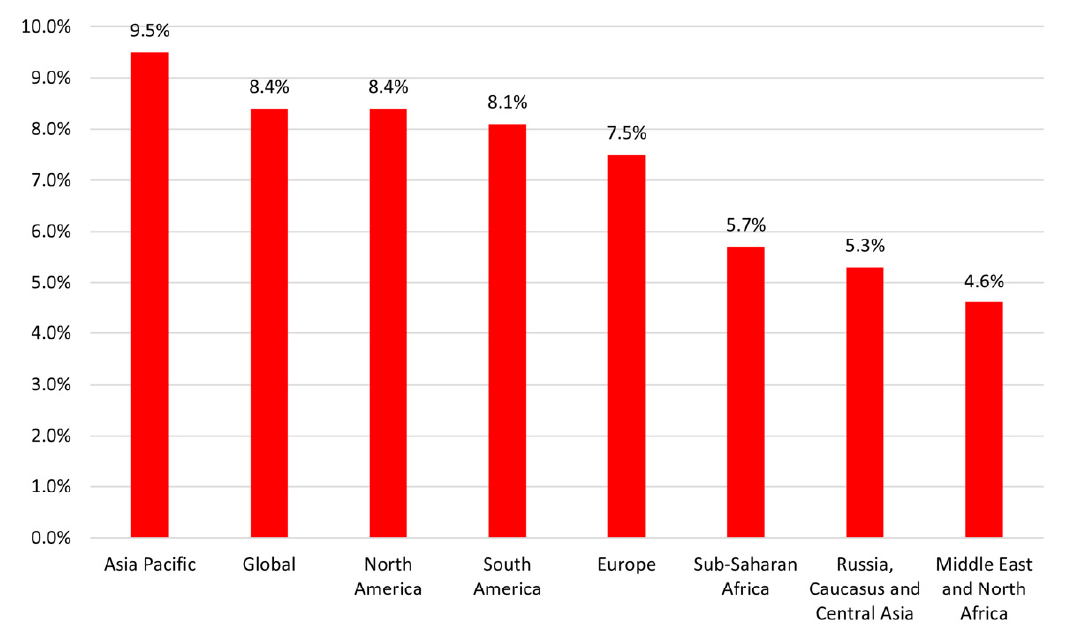

The global contract logistics market expanded 10.9% during the first six months of 2020 as countries across the world emerged from the grips of Covid-19, showing signs of a fragile recovery. Ti’s latest forecast data shows a moderately slower pace of expansion over the full year 2021, with 8.4% growth expected. Ending 2021 with a total value of €237.5bn, the global contract logistics market has a CRT21 rating of 4.8%, having more than offset the declines seen in 2020.

Globally contract logistics market development in the first half of 2020 has been vigorous. Some 11 countries (of 25 for which H1 2021 market sizes are provided) have seen double-digit expansions during the period, in large part driven by the lessening of pandemic-related restrictions on social and economic activity as well as the drive to vaccinate populations. In addition, the easing of pandemic effects has been boosted by government spending which supported jobs and household incomes. In the US and Europe particularly, government support has elevated consumer spending power to provide retail, and the wider services industry, much-needed demand during reopenings. In the US, for example, Covid relief and support payments have helped preserve household spending and push saving rates to meaningfully higher levels – at 9.6% in July, the personal savings rate is higher than its 7.3% average since 1980. This is helping drive retail sales up, with e-commerce sales 9.1% higher in Q2 2021 than a year earlier and totalling 13.3% of all retail sales.

There are, however, notable headwinds to recovery. Supply bottlenecks are prevalent in all strategic contract logistics sectors on a global basis, while the spread of the delta variant of Covid-19 is already seeing new lockdowns. The potential for further restrictions looming and is damaging confidence amongst both consumers and businesses, curtailing demand and investment. In Germany, for example, ongoing chip shortages are a lingering concern for BMW, which states problems will last into at least 2022, and Mercedes, where shortages could cause delays into 2023. Indeed, supply bottlenecks have seen backlogs of work rise as stock levels have fallen, resulting in price pressures across the German manufacturing sector while output growth is further behind new order growth than at any point in the 25 years of PMI records.

The development of the global contract logistics market is then almost as much about the evolution of the Covid-19 pandemic as it is about any newfound dynamism or drivers of growth in the global economy. The mix of manufacturing, production, retail and consumer spending growth that is driving the market remains, in many cases, vulnerable to the supply constraints that stem from pandemic disruptions, with the lingering threat of new infection waves providing further concern about how, when and where supply chain vulnerabilities may again be exposed. It leaves the question, how much of the momentum in 2021 can be considered “growth” and how much is better characterised as “recovery”.

Growth is not so dynamic in other regions. In Europe, the Big Five economies are, at the end of 2021, forecast to show only marginal improvements over pre-pandemic scale. Contract logistics markets in Spain (0.3%), the UK (0.7%) and France (0.7%) offer the most anaemic CRT21 figures, while Italy (1.1%) shows better performance but has the greatest ground to recover following deep effects of the pandemic, particularly early in 2020. Germany (2.1%) shows strong growth potential, although it weathered the pandemic effects better than its peers and grows from a higher base, as it also faces headwinds related to the global supply of chips and semiconductors which threaten to undermine growth in the all-important automotive manufacturing sector.

Contract Logistics Market Growth – 2021 Region Forecasts

Source: Transport Intelligence, October 5, 2021

Author: Ti Insight

This brief has been taken from a larger paper, ‘Global Contract Logistics Market Forecasts for 2021 and 2025: a fragile recovery’ by Ti Insight. This paper is available exclusively to GSCi subscribers. Each week, Ti’s team of senior analysts and industry experts deliver analysis covering the latest logistics and supply chain trends exclusively to users of GSCi.