Trends in air and sea freight did not offer comfort to industry players, with IATA forecasting a “disappointing” year for air cargo, and container shipping rates hitting new lows.

IATA data showed that global air cargo traffic grew by a mere 0.9% in May 2016, with European growth counterbalancing declines in Asia and North America. Yields were weakened once more, as capacity grew by 4.9% compared to the previous year.

In containerized sea freight, there are suggestions that freight rates are bottoming out. According to Drewry, the price of transporting an FEU from Asia to the US West Coast has hit $800, whilst the Chief Commercial Officer of Maersk subsidiary MCC Transport has observed intra-Asia freight rate declines of as much as 30%. Commenting to The Loadstar, he stated: “This is simply not sustainable.”

Meanwhile, the Panama Canal has re-opened to traffic, allowing the transit of so-called ‘Neo-Panamax’ vessels of up to 14,000 TEU in size. The implications of this are greater competition between East and West Coast ports in the USA, though many of the former are not yet ready for the larger ships. As The Wall Street Journal reported in June, the Port of New York and New Jersey is constrained by the height of the Bayonne Bridge, for example.

Alliance activity continues in the industry, with Hyundai Merchant Marine mooted to be joining the 2M Alliance, with suggestions that it will be joined by Israeli carrier Zim. Nonetheless, actions to reduce capacity are now at the forefront of many minds.

![]()

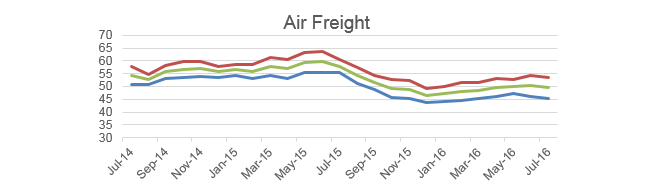

Air freight

Following a period of upward momentum, the air freight Index declined for the second month in a row. The Index fell by 0.8 points month on month, and by 8.4 points year on year. It is 4.8 points below the result for July 2014.

The present situation results fell by 0.7 points to 45.5. Three of the four lanes recorded month on month declines, the exception being the Europe to Asia lane, which gained 2.1 points to 43.9. Asia to Europe lost 2.5 points to 45.9, whilst Europe to US and US to Europe lost 1.3 and 1.5 points, to 47.2 and 45.1 respectively.

The air freight logistics expectations Index fell by 0.8 points to 53.7, with declines across the board. The greatest of these was Europe to Asia, which fell by 1.6 points to 51.5. Meanwhile, Europe to US lost 0.6 points to 51.9. Asia to Europe and US to Europe each lost 0.5 points, falling to 55.5 and 55.9 points, respectively.

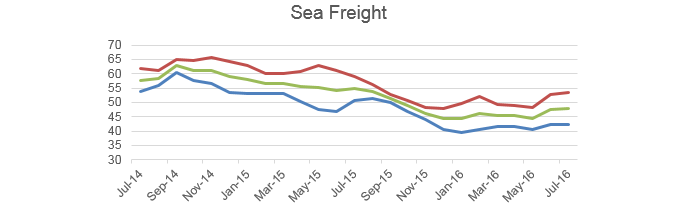

Sea Freight

For July, the sea freight logistics confidence Index improved by 0.3 points to 47.9. This rise was chiefly drawn from the expected situation Index, though the present Index also rose slightly.

Standing at 42.3, the present sea freight Index remained negative, as were all four individual lanes surveyed. Only one lane, Europe to Asia, registered an improvement for the month, increasing by 3.8 points to 38.4. Of the remaining lanes, US to Europe declined by 1.8 points to 38.2, representing the lowest scoring lane surveyed. Asia to Europe declined 1.2 points to 45.1, whilst Europe to US fell 0.6 points to 47.5.

The sea freight expected Index rose at a slightly greater rate of 0.5 points to 53.4, though the picture amongst the lanes was mixed. Europe to US rose by 1.9 points to 55.1, and Europe to Asia gained 1.5 points to 50.1. In contrast, US to Europe lost 1.5 points to total 50.8, and Asia to Europe contracted by 0.1 points to 57.2.

![]()

One-Off Question

The one-off question for July cited the positive outlook registered in the June survey, to ask participants what they believed to be driving the improvement in the outlook.

There was no clear majority. Nonetheless, the largest respondent group, with 30.6% of survey participants, stated that the outlook was good simply because it coincided with the 2016 holiday season. Regardless, a slightly smaller group, 26.5% of respondents, attributed the climb to a more general improvement across both Europe and other markets.

Of the remaining respondent groups, 20.4% believed the outlook to be derived from an expected improvement in European markets specifically, whilst 16.3% instead cited expected improvements in other markets as the main cause. The remaining 6.1% asserted a range of alternative answers, including the 2016 US Presidential election.

Source: Transport Intelligence, July 12, 2016