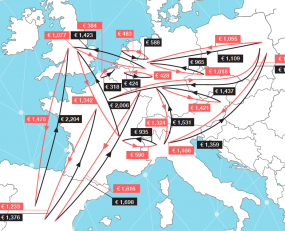

Ti and Upply’s European Road Freight Rate Benchmark Q1 2021 shows that rates have increased amid the disruption of Brexit and new lockdowns across Europe as businesses work to keep moving under pressure.

Despite hopes for a strong economic performance at the turn of the year, Europe has suffered due to surging COVID-19 case levels. Vaccination attempts so far have largely been insufficient to halt the spread of the virus, which has led to new or extended lockdowns and public health restrictions. This has slowed the economic recovery, despite lockdowns being less economically intrusive than early last year. Consumer confidence has suffered, leading to restrained import demand.

However, there has been a recovery in global trade levels, which is aiding the European market. Rising demand levels from other regions, notably the US and China, is benefitting intra-European manufacturing supply chains. This is providing some impetus for demand in the market. Supply chain disruption has been a key feature of the early part of 2021 and this appears to have been priced in by hauliers. Increasingly, drivers travelling across borders are being required to carry out COVID-19 tests or expected to queue as such checks are carried out. Shortages in the air and sea freight markets are leading to longer lead times, whilst there also appear to be shortages in some commodities and components such as semiconductors. These constraints appear to have tipped the balance of pricing power towards hauliers.

The new benchmark report also shows how Brexit has brought about severe challenges for hauliers crossing the English Channel. Paperwork issues have been common, with just under 40% of respondents in an ONS survey identifying this as the main hurdle to cross-border trade. Some hauliers appear to have avoided crossing the border altogether at times. This has squeezed capacity and led to higher costs, which in turn has led to higher rates, with an increase of 1.3% quarter-on-quarter and 5% year-on-year. However, with depressed demand, hauliers appear to have been cautious in rate pricing early on. According to the ONS, UK exports to the EU fell 40.7% year-over-year in January, with imports down 28.8%. Trade has since improved, but still sits below February 2020 levels.

The data supporting the latest benchmark report also shows that rates in the countries harder hit by Covid-19 are beginning to recover and catch up with those in the countries less hard hit. For example, Germany has handled the pandemic better than most European countries, although unfortunately it has been hit by a new wave of infections in Q1 2021 leading to German rates falling 0.4% quarter-on-quarter, but ex-German rates have grown by 1.3% closing the gap in rates back towards pre-pandemic levels.

Andy Ralls, Quantitative Analyst at Ti, commented, “Rates only rose moderately in Q1, with demand held back by the new wave of COVID-19 infections across Europe. Like in early 2020, this led to lumpy demand patterns, which skewed fronthaul-backhaul rate dynamics on a number of lanes. However, Brexit disruption, rising diesel prices and an increase in global trade volumes make further rate rises likely in the months ahead”

Thomas Larrieu, Upply’s Chief Data & Research Officer, comments: “In the coming months, we can expect an improvement in the health situation in Europe thanks to the vaccination campaigns. In addition, the economic support plans will gradually take effect. We can therefore expect a recovery in consumption in Europe, and consequently in the demand for transport. Freight rates should therefore continue to rise in Q2 2021, especially as inflationary trends on oil should also influence transport prices upwards. That said, there is still a lot of uncertainty in the very short term, as the Covid-19 epidemic remains very active.”

Source: Transport Intelligence, May 4, 2021

Author: Transport Intelligence

About the European Road Freight Rate Benchmark

The European Road Freight Rate Benchmark report is designed to provide greater visibility of freight rate development across Europe. It will be available to download from Wednesday 5th May.

You can also join Ti and Upply for the European Road Freight Rate Development Benchmark Webinar, Wednesday 5th May 2021, 15:00 CET. All registrants for the webinar will also be sent a free copy of the benchmark report.

The Webinar will feature Thomas Larrieu, Upply’s Chief Data Officer; William Béguerie, Road Transport Expert for Upply; Andy Ralls, Quantitative Analyst at Ti; and Michael Clover, Ti’s Head of Commercial Development, discussing the data trends and drivers behind:

CLICK HERE to register for the webinar at 15:00 CET on Wednesday 5th May.

CLICK HERE to download a copy of the full benchmark report.

If you have any questions about the report please contact Michael Clover, Ti’s Head of Commercial Development – [email protected].