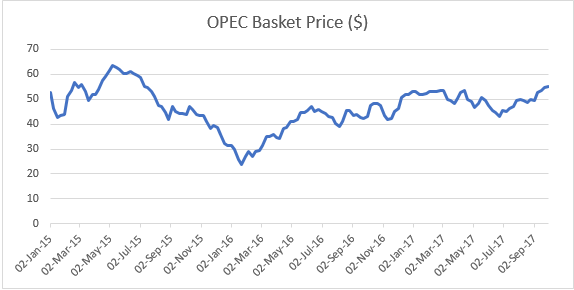

Ti’s latest weekly tracker of the OPEC basket price of oil shows that barrels were up at a two year high this week, surpassing $55. The basket price has also shown the largest third quarter percentage gain for 13 years.

The volatile nature of oil and fuel prices is a common concern for LSPs. For European road freight providers for example, around 25-40% of costs for a HGV is represented by expenditure on fuel, but should they really be worried about an increase in oil prices?

It is first useful to consider the reasons for the increase. The latest spike appears to have been as a result of political instability, a common cause of oil price rises. Following the Kurdish referendum, Turkey’s President Recep Tayyip Erdogan threatened to cut off a major pipeline that flows from the Kurdish region in Northern Iraq.

In the slightly longer term, demand has risen and following OPEC’s cuts earlier in the year, global supplies have flatlined. The price has also been at extremely low levels over the last few years and it is worth noting that the 3rd quarter of the year tends to be quite strong.

This growth only represents a relatively small recovery since its crash in 2014 though. Since then, the industry has had to adapt to a world of low oil prices, often beneath the psychological barrier of $50 a barrel. Despite this, road transport providers have still looked to develop alternative fuel strategies, with environmental impact and regulations in mind, slowing their demand for oil.

Look at “the big 3” express providers as a global example. FedEx have improved total fleet miles per gallon in the US by 14.1% since 2015. DHL and Ford jointly produced the “StreetScooter Work XL”, an e-van with a Ford Transit chassis. They hope to build 2,500 e-vans by the end of 2018. UPS meanwhile claim to operate one of the largest private alternative fuel fleets in the US, with more than 5,088 vehicles including all-electric, hybrid electric, hydraulic hybrid, CNG, LNG, propane, biomethane and light-weight fuel-saving composite body vehicles.

These companies, and many others, are showing sincerity in their search for alternative fuel arrangements. Their concern with oil is therefore beginning to reduce.

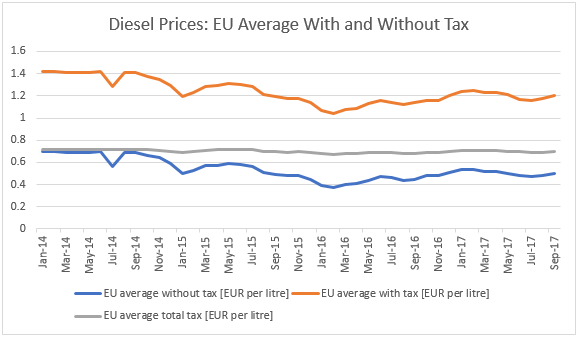

Also, diesel prices are moderated quite well by taxes. As shown in the graph below, approximately half of the cost of EU diesel is accounted for by tax, which is a relatively constant, almost fixed, addition to fuel price.

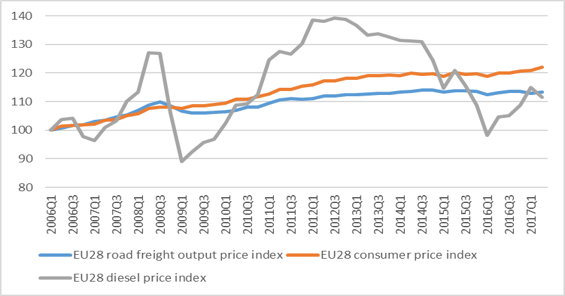

Even when these prices do move, the shock is not as significant as one may think. As previously stated, fuel prices make up a relatively high proportion of road transport company’s costs. Increases and decreases in prices do make a difference, but it is only very large fluctuations that seem to have a material impact on freight rates. The European road freight market is highly fragmented, which in turn restrains price growth.

Road carriers are continuing to diversify their fleets to utilise alternative fuels and rates are altered by a number of other factors. A jump in oil prices, which has been expected for some time anyway is therefore not as disruptive as perceptions suggest.

Source: Transport Intelligence, October 3, 2017

Author: Andy Ralls

If you’d like to have your say on the state of the European Road Freight market in 2017, and to receive a copy of Influential Technology Trends in 2017 and a 25% discount on the European Road Freight Transport 2017 report when published, please click here to take our survey.