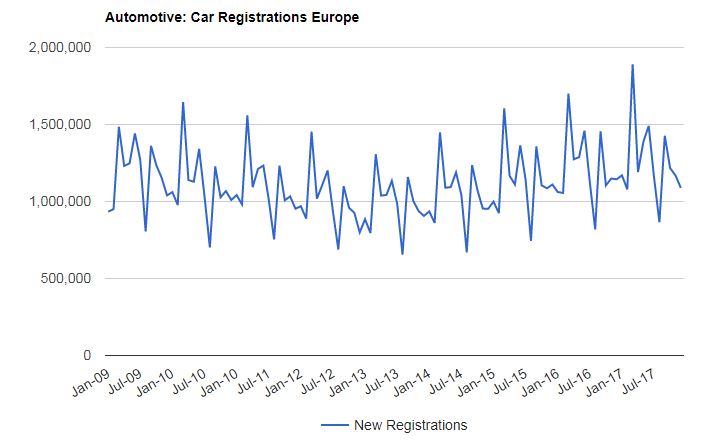

2017 was generally a good year for European automotive logistics providers. Registrations of new passenger cars in Europe grew by 3.4% in 2017. This represented the fourth consecutive year of increases, and at over 15m, new vehicle registrations are at their highest level since 2007.

Source: ACEA

Improving global economic conditions undoubtedly helped sales but regulations prohibiting the use of diesel cars have hit manufacturers’ top line figures. Still, the vast majority have expanded sales volumes. Most notably, Europe’s second biggest player, PSA Group, recorded a 28.2% increase in units sold. Their major LSP, GEFCO, is bound to have prospered as a result.

Delving further into the figures presented by the ACEA, growth is seen across the majority of the continent. It is unsurprisingly strongest in Eastern and Baltic States where Lithuania (+27.3%), Hungary (+20.4%) and Bulgaria (+18.5%) lead the way.

Sales in France grew by 4.7%, which has recently seen some key acquisitions in automotive logistics. Most notably, Groupe CAT purchased STVA, one of the largest handlers of finished vehicles in Europe, from SNCF. Groupe CAT has also taken over Carlson, Trial, Fleetpoint, CSE, Toquero and Sintax in recent years as it aims to grow revenues to over €2bn by 2020.

Sales volume growth in Germany was on the lower end of the European spectrum (+2.7%). Emissions have been a highly contentious point for consumers in Europe’s largest market and sales of diesel cars were down 13% in 2017. This came off the back of VW’s emissions scandals and threats of penalties by the EU on dozens of German cities for high pollution.

In Italy, tax incentives helped increase sales to businesses by around 30%. This led to an increase in new passenger car registrations of 7.9%. Meanwhile Spain’s growth of 7.7% can in part be attributed to the success of its largest carmaker Seat, which sold 23.1% more vehicles in Spain in 2017. After a complete revamp of its supply chain after the financial crash, its main facility in Matorell, near Barcelona, is now close to maximum capacity.

Interestingly, UK demand was down for the first time in six years (-5.7%). Mike Hawes, Society of Motor Manufacturers and Traders (SMMT) Chief Executive, commented that “falling business and consumer confidence is undoubtedly taking a toll”. In November 2017, a Parliament select committee heard that every 15 minutes of customs delays could cost some manufacturers up to £850,000 a year after Brexit. Furthermore, once the UK leaves the single market, type approvals issued by the VCA, which allow UK manufacturers to sell into the EU, will no longer be valid. Carmakers have warned that this could result in production grinding to a halt. It is not yet clear how (or if) this obstacle can be resolved.

Despite another year of higher sales volumes, growth in 2017 was the weakest it had been for the last four years. Brexit is an issue that looms over not just the UK automotive sector, but also the parts manufacturers that sell into it. The move away from diesel and towards electric vehicles provides challenges for existing players in the market and, as we head into 2018, finished vehicle inventories are gradually rising. The outlook for the car industry in Europe is less rosy than its recent trajectory suggests.

Source: Transport Intelligence, January 30, 2017

Author: Andy Ralls

For more industry-wide data, as well as information on key providers, markets, vertical sectors and geographies, please visit Ti’s new Global Supply Chain Intelligence platform.