The Chart of the Month for December focuses on NAFTA trade data provided by the US Bureau for Transportation and Statistics (BTS). Renegotiations for the 23-year old free trade deal are ongoing and 2018 is set to be a decisive year.

Free trade advocates are understandably concerned about the possible outcomes of the renegotiation. The Trump administration is aiming to boost US manufacturing and jobs, but many have suggested that its approach could backfire.

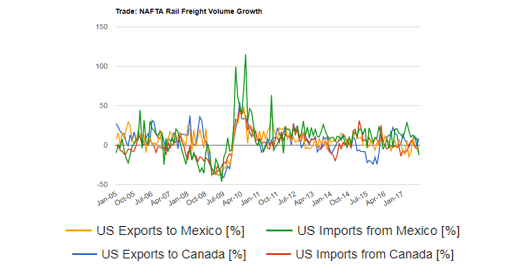

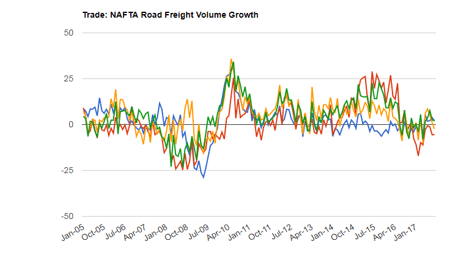

The integration of supply chains across borders has boosted volumes for North American road and rail freight operators. The BTS provides volume growth data on these North American trade lanes over the last 12 years.

The graphs, new to the Ti Dashboard, measure the value of trade crossing borders over time, but strip out the effects of inflation and currency movements, meaning fluctuations are only driven by changing volumes. They show the volatile nature of trade between the US and its neighbours, particularly in rail freight volumes. Even taking the economic crash out of the equation, when measured monthly, double digit year-over-year percentage changes are commonplace.

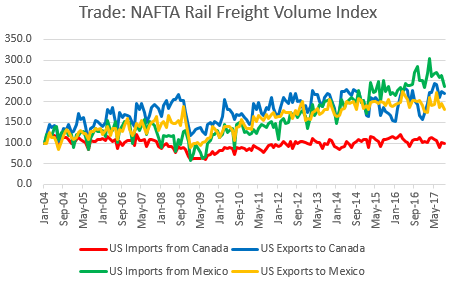

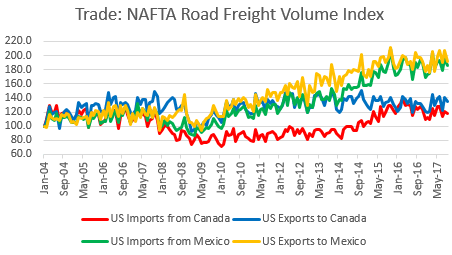

Viewing the data in index form, a clear long-term growth pattern in Mexican trade is visible.

Interestingly, US exports by road to Mexico have grown more strongly over the longer term than imports. Exports grew at a 12-year real compound annual growth rate (CAGR) of 4.7%, with imports at 4.4% (these figures take an average of the index in 2004 and in 2016). Over the past five years however, the story is reversed, and growth has accelerated in both directions (imports: 8.5% exports: 6.7%). By rail, US imports from Mexico have been ahead of exports (12-year CAGRs of 5.9% and 5.1% respectively). Over the last five years, the gap between imports and exports has widened, to 12.2% and 4.9% respectively.

US overland trade with Mexico has consistently performed better than the United States’ overall international trade. With a small exception in the case of US exports by rail to Mexico, other lanes have seen stronger growth rates over the past five years, at a time when US international trade has witnessed a slowdown.

Canada, however, is a different story.

Remarkably, the US imports less (in volume terms) from Canada via rail than it did 12 years ago. Volumes do not appear to have shifted to road either, which has only grown at 0.7% per year. Part of this has been due to the slowdown in bulk shipments, including forest products and minerals travelling cross-border. Over the past five years however, its real CAGRs for rail and road have picked up to 3.9% and 8.0% respectively.

US exports to Canada via rail and road have grown at 12-year real CAGRs of 3.7% and 1.1% respectively. Over the past five years, the corresponding CAGRs are 2.1% and 0.0%.

In summary, NAFTA renegotiations come at a time where US overland imports are growing substantially, ahead of their milder longer-term trend. US exports to Canada are wavering, but to Mexico, they remain ahead of average US export growth. If the negotiations force up trade barriers next year, expect to see drastic changes to these charts.

Source: Transport Intelligence, December 5, 2017

Author: Andy Ralls