DHL released an interesting report investigating opportunities in cross-border e-commerce, with some very interesting findings.

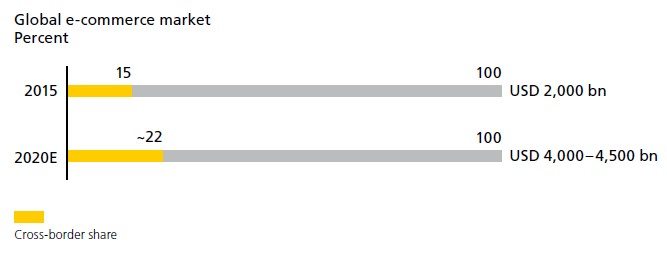

The first is that cross-border e-commerce accounted for 15% of global e-commerce sales in 2015. That proportion is set to rise to approximately 22% by 2020. Secondly, cross-border e-commerce is expected to grow by around 25% annually until 2020, nearly twice the rate of domestic e-commerce.

Development of cross-border e-commerce share (2015-2020E)

Source: Alipay, Mckinsey; taken from DHL report

What do these numbers tell us about the global e-commerce logistics market?

It is tempting to think that cross-border e-commerce logistics must represent a greater than 15% share of the market, the present share of global cross-border sales. Logistics costs associated with the average cross-border shipment are surely higher than the average domestic shipment. On the shipping side, the average distance travelled is likely to be much further, and may often require relatively expensive air transport. Cross-border goods are also associated with premium shipping. DHL states that every tenth US dollar of cross-border e-commerce revenue is made through a time-definite premium shipment. In addition, on the warehousing side, cross-border products are often more slow-turning than domestic goods.

However, what is crucial to realise is that the average value of a cross-border shipment is also typically considerably higher than a domestic shipment. DHL’s conservative estimate is that 10 to 20% of all cross-border transactions exceed $200, “a higher share of high-basket-value sales than in any domestic e-commerce market.”

In summary, domestic shipments are relatively low-logistics cost and low-value, whereas cross-border shipments are relatively high-logistics cost and high-value. It is not clear whether logistics costs as a % of sales are higher for the average domestic e-commerce shipment or cross-border shipment. This is one facet of e-commerce logistics cost structures that cannot yet be understood clearly.

There are many that can be though. For example, in Ti’s latest report Global e-commerce Logistics 2017, logistics costs as a % of sales have been benchmarked for over 20 different online retailers. Conclusions have been drawn on how logistics costs as a % of sales tend to vary by vertical sector, retail channel and geography. These have been benchmarked against store-based retailers’ logistics costs. The division of warehousing and fulfilment costs for a number of online retailers has also been identified.

Overall, there are a huge range of factors that influence e-commerce logistics costs, some of which simply can’t be reasonably quantified or understood. However, among the factors that we can identify, such as how and why logistics costs vary by vertical, retail channel and geography, it is possible to put together enough pieces of the jigsaw to get a comprehensive understanding of e-commerce logistics cost structures.

Source: Transport Intelligence, originally published February 7, 2017

Author: David Buckby