|

Note to reader: This article should take about 6 minutes to read but we have marked the approx 2 minute mark. |

Author: Prof John Manners-Bell

The container shipping industry has been through a very traumatic few years with huge losses incurred by many of the market leaders. The underlying problems for the industry have come about fundamentally due to overcapacity in the market and weak global economic growth. At the time of its results in early 2017, Maersk commented that market capacity had been expanding by 7-8% in 2015 at a time when demand was significantly less than that.

This imbalance in supply and demand had serious consequences for the sector resulting in the bankruptcy of a top ten carrier, Hanjin Shipping. Smaller market players have been acquired by competitors and others forced to go cap in hand to governments for emergency loans (e.g. Taiwanese carriers Evergreen and Yang Ming).

It is some comfort to the sector that rates and volumes now seem to have revived and Maersk, Hapag-Lloyd and CMA CGM have all suggested that full year 2017 results will be much better than those in 2016. This will be helped by the growth in new container capacity being brought to market slowing to an annual rate of just 2%. Despite this, parts of the market still struggle and it is likely that there will be further consolidation in the market in the years to come. This briefing will provide insight into many of the major trends impacting on the industry including:

HOW CONSOLIDATED IS THE GLOBAL SHIPPING SECTOR?

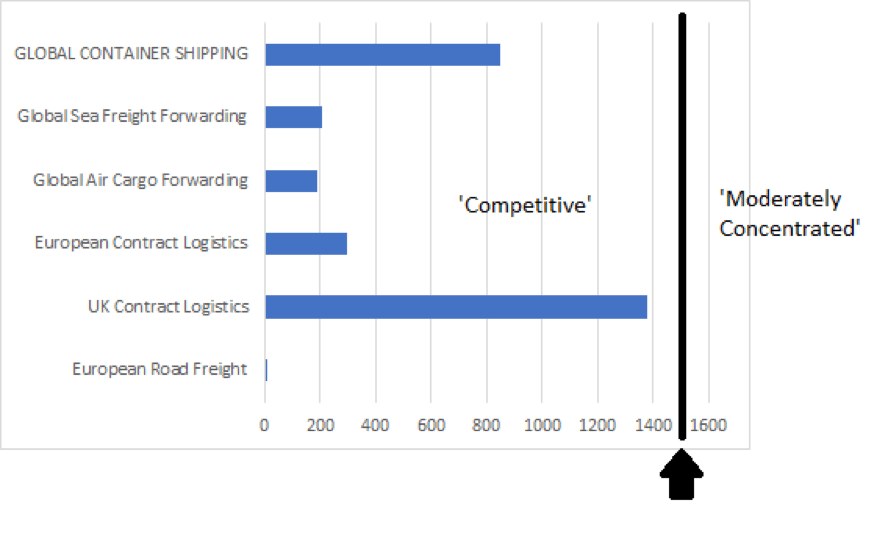

The low profitability and returns on investment have been the most powerful driver of consolidation within the shipping industry. One way to objectively assess the extent to which the market has become consolidated is by using the Herfindahl-Hirschman Index (HHI) of market concentration. Looking at Figure 1 it can be seen that the global shipping market is still defined as ‘competitive’ (less than 1500) but that only refers to the global market as a whole and not specific lanes. The issues of Alliances (dealt with below) complicates matters further.

Figure 1: Herfindahl-Hirschman Index for logistics sectors

In comparison with a selection of other logistics sectors, the container shipping market is far more consolidated, with the exception of the UK contract logistics industry. This of course does not necessarily mean that the result is higher rates, although the relative lack of competition can be a factor.

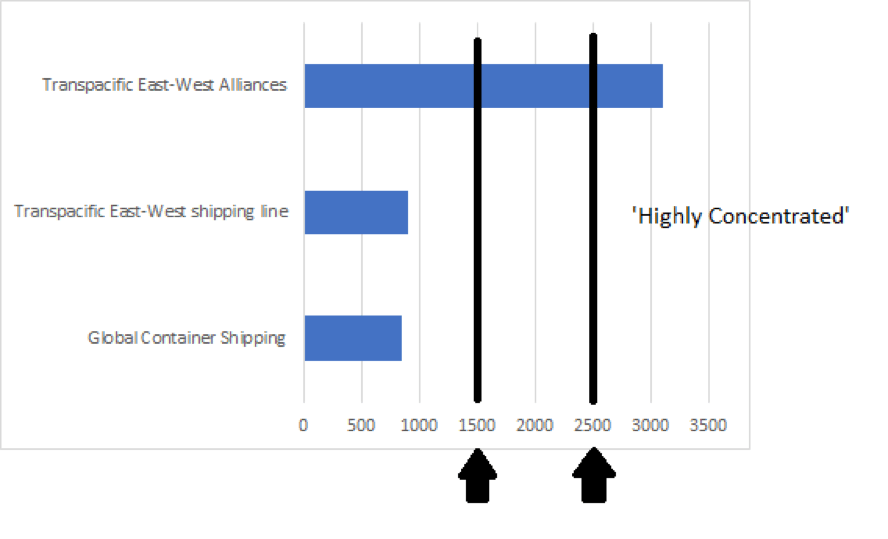

Figure 2: Herfindahl-Hirschman Index for Transpacific East-West Trade

Looking specifically at the Transpacific East-West trade lane, it can be seen that by calculating the HHI for individual shipping lines, the market is still regarded as ‘competitive’. However, by looking at the trade lane in terms of the market share of Alliances, it is now regarded as being ‘Highly concentrated.’ Alliances are, in theory, designed to provide ‘pre-competitive’ exemptions to anti-trust regulations. That is to say, pricing, marketing and selling will remain independently managed by each of the shipping lines whilst vessel sharing and joint services are allowed. The present set of Alliances has been agreed by the relevant competition authorities which, in the case of the US, is the Federal Maritime Commission (FMC) although this has not prevented what could be described as a policy dispute amongst regulators.

In a letter dated November 2016, the US Department of Justice (DoJ) wrote to the Secretary of the FMC. In it the Assistant Attorney General warned, ‘THE Alliance Agreement raises a number of significant competitive concerns, particularly as it comes on the heels of the recently approved OCEAN Alliance. The creation of these two new alliances will result in a significant increase in concentration in the industry as the existing four major shipping alliances are replaced by only three. This increase in concentration and reduction in the number of shipping alliances will likely facilitate coordination in an industry that is already prone to collusion.’

So, it can be seen that at the highest level there are concerns about the impact of Alliances on the competitive functioning of the shipping market although this has been denied by shipping lines themselves. From their perspective Alliances can provide their customers with:

There are, however, risks for the lines themselves as Alliances may lead to the commoditization of services and products. It is obviously impossible to compete on speed of service, for example, with a fellow Alliance member as the container will be carried on a shared vessel.

From a risk perspective, shippers have been urged to consider booking on separate Alliances rather than just separate lines if they want to ensure that their containers go on separate vessels.

A RECENT HISTORY OF SHIPPING INDUSTRY CONSOLIDATION

Since the ‘Great Recession’ of 2008/9 there has been significant consolidation in the shipping industry although this did not happen immediately. The fall out at the time was not as great as many predicted due to many shipping lines, which fell into the category ‘national flag carriers’, being propped up by governments. At the time Ti’s Lead Analyst, Thomas Cullen, concluded:

‘This trend to resist rationalisation of capacity is likely to amplify the structural problems of the container sector. The recovery in volumes is anaemic whilst changes in trade-patterns are likely to make the situation worse. If, added to this, governments resist consolidation, there will be on-going structural over-capacity. It might be logical to ask if the effect of such behaviour would be the creation of ‘zombie’ shipping companies, operating far more capacity than they can operate economically.’

The uneconomic and weakened nature of many shipping lines was laid bare when Maersk, followed by many of its competitors, embarked on massive new building strategies, increasing significantly the size of their vessels. This resulted in much greater economies of scale, driving down their cost base and providing them with substantial competitive advantage. Only those with the deepest pockets could follow Maersk and those who couldn’t, or those who over-extended themselves in their efforts to compete, became targets for acquisition or indeed, in the case of Hanjin, failed completely.

As can be seen from the tables developed from figures provided by Alphaliner, there has been significant consolidation in the market since 2015.

Figure 3: Shipping Line Market Share 2014 v 2017

|

Rank |

Shipping Line |

Market share 2017 |

|

1 |

Maersk |

19.3% |

|

2 |

MSC |

14.7% |

|

3 |

CMA CGM |

11.7% |

|

4 |

COSCO |

8.5% |

|

5 |

Hapag-Lloyd |

7.1% |

|

6 |

ONE (NYK, K Line, MOL) |

6.7% |

|

7 |

Evergreen |

5% |

|

8 |

OOCL |

3.2% |

|

9 |

Yang Ming |

2.7% |

|

10 |

PIL |

1.7% |

|

|

Total Top Ten |

80.6% |

|

Rank |

Shipping Line |

Market share 2015 |

|

1 |

Maersk |

15.5% |

|

2 |

MSC |

13.5% |

|

3 |

CMA CGM |

8.8% |

|

4 |

Hapag-Lloyd |

5.2% |

|

5 |

Evergreen |

5.1% |

|

6 |

COSCO |

4.4% |

|

7 |

China Shipping |

3.6% |

|

8 |

MOL |

3.2% |

|

9 |

Hanjin |

3.2% |

|

10 |

APL |

3.0% |

|

|

Total Top Ten |

65.5% |

Whereas the Top Ten accounted for 66% of the market in 2015 this had risen to 81% in 2017. The key events are detailed in the Figure 4.

Figure 4: Recent mergers and acquisitions and failure

2017 Merger NYK, Mitsui OSK and K-Line (ONE)

2017 Acquisition Maersk acquires Hamburg Sud

2016 Acquisition Hapag Lloyd acquires UASC

2016 Acquisition CMA CGM acquires NOL

2016 Bankruptcy Hanjin goes bankrupt

2016 Merger Cosco and China Shipping

2014 Acquisition Hapag Lloyd acquires CSAV

The clear direction of the sector is towards consolidation around a few large players, which should mean that they will be able to exercise some control over the availability of capacity on the market. As regards future M&A, there is the possibility of a merger between Evergreen and Yang Min (although denied by the lines themselves and made difficult by the debt burden of both companies). The Chinese will not be allowed to buy these Taiwanese companies which would also limit consolidation.

Hapag Lloyd may be interested in further acquisitions to complement its strength in north-south trades but only if the various shareholders have the money. Plus, there are strong reasons to believe that Hapag itself will become a target in the next year or so.

There is a view that consolidation has reduced rate volatility but this has come at quite a cost to the shipping lines which have loaded up with debt to make the acquisitions.

ALLIANCES

2017 has also seen the advent of a new structure of Alliances which, along with acquisitions, have also served to manage capacity. The new Alliances came into effect as many of the previous alliance arrangements had collapsed in the face of the consolidation and the bankruptcy of Hanjin. The previous four (G6, CKYE, 03 and 2M) were replaced by three, larger alliances (2M, Ocean Alliance and THE Alliance). These alliances now account for about three quarters of global container capacity and almost all the capacity on East-West trade.

As has been indicated, capacity is more concentrated than at the time the outline of the former alliance structure was created, with the big players now having more dominant market shares. It should be remembered that these alliances do not account for the whole fleets of the companies concerned. The larger lines in particular can put vessels on routes not covered by the alliances.

One of the implications of the changes is an increase in the average size of vessels available. One of the attractions of alliances is that medium-sized shipping lines find the opportunity to deploy their largest ships. If this is the case, this may suggest that available capacity will also increase.

2M is the largest alliance (33% global capacity). It is made up of:

The second largest (26% global capacity) is the Ocean Alliance consisting of:

The rival ‘THE Alliance’ (16% global capacity) is made up of:

The ‘2M’ Alliance between the largest container shipping lines, Maersk (including its acquisition Hamburg Sud) and MSC, accounts for about a third of available global capacity although figures are complicated by the fact that HMM has attached itseld to the 2M Alliance as a junior member through a Vessel Sharing Agreement rather than as a full partner. It will continue to operate Asia-US West Coast services itself whilst selling some of its capacity to its 2M partners. Likewise, it will purchase slots on Asia-Europe and Asia-US East Coast from Maersk and MSC.

It is perceived that the ‘Ocean Alliance’ is the stronger player of the two new alliances. For example, the shipping data provider Alphaliner estimates that the ‘Ocean Alliance’ has 35% of the capacity on the East-West trade routes whilst the ‘THE Alliance’ has 27% (2M, 33%). 2M has the greatest market share on Transatlantic and Europe-Far East routes whilst Ocean dominates the Trans-Pacific trades.

THE ROLE OF CHINESE INVESTMENT

Whilst at the same time that the container shipping industry is undergoing a period of rationalization and cost-cutting, the Chinese state appears to be pouring money into the sector.

The China Ocean Shipping Company, or COSCO, which is a Chinese ‘State-owned Enterprise’ announced in January 2017 that it had “established a long-term cooperation mechanism […] with the China Development Bank with the objective of serving “the national strategy of ‘all the way along the way’, ‘marine power’ and ‘manufacturing power’ and ‘deepening reform of state-owned enterprises’”. This appears to refer to the ‘One Belt One Road’ concept that the Chinese government has for developing Central Asia and linking China to markets in Europe.

The agreement seems to provide funding through various types of financial products, possibly to a total of CNY180bn, although there is some mention of “co-financing”. This a huge amount of money, roughly equivalent to US$26bn. The implied time scale of the deal is over a period of the next four years.

Bearing in mind the size of the sum involved this would suggest the construction of very substantial port infrastructure on the route, as well as, presumably, investment in container shipping. If only part of this lending facility were accessed, the implications for the entire container sector would be significant. It is also tempting to think that in the short-term a debt fuelled COSCO will grasp the opportunity to buy some distressed container shipping assets.

THE LONG VIEW

Taking the long view on shipping, traditionally the industry has been characterized by boom and bust. Writing in his book ‘Shipping Futures’ in 1987, the author, James Gray says, ‘Every time demand exceeds supply, even if that imbalance is known to be temporary, there is a rush of new building orders…a curiously short-sighted but overwhelming desire on the part of banks to lend money for maritime enterprises, and sooner or later the inevitable collapse… We seem as an industry consistently to get the long-term pattern wrong.’

There is little evidence to suggest that 30 years later anything much has changed especially given the grim year recently experienced by shipping lines, but now largely forgotten. It is still to be seen whether shipping lines will be able to contain their enthusiasm for ever-larger new build ships when the global economy recovers fully. It would seem likely that there will be further consolidation of the industry in the short/medium term with many mid-sized players struggling to compete against the market leaders even if they are operating within major alliances.